Decree No. 05/2009/ND-CP of January 19, 2009, detailing the implementation of the Ordinance on Royalties and the ordinance amending and supplementing article 6 of the Ordinance on Royalties. đã được thay thế bởi Decree No. 50/2010/ND-CP detailing and guiding a number of articles of the Law o và được áp dụng kể từ ngày 01/07/2010.

Nội dung toàn văn Decree No. 05/2009/ND-CP of January 19, 2009, detailing the implementation of the Ordinance on Royalties and the ordinance amending and supplementing article 6 of the Ordinance on Royalties.

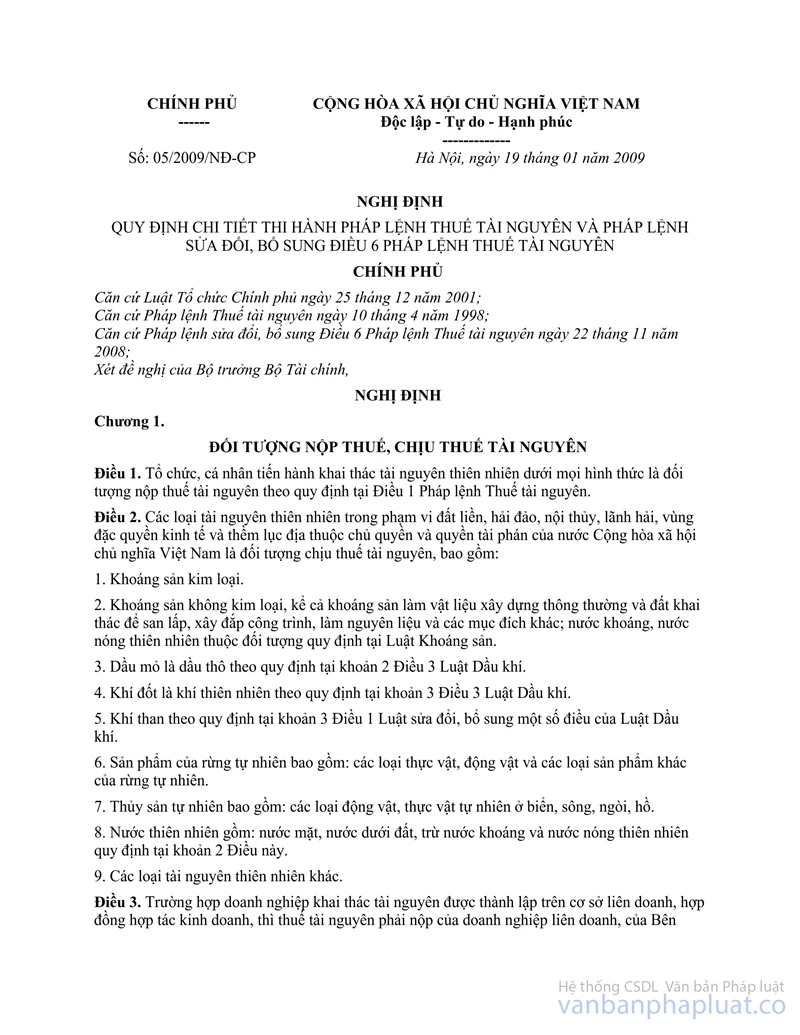

THE GOVERNMENT | SOCIALIST REPUBLIC OF VIET NAM |

No. 05/2009/ND-CP | Hanoi, January 19, 2009 |

DECREE

DETAILING THE IMPLEMENTATION OF THE ORDINANCE ON ROYALTIES AND THE ORDINANCE AMENDING AND SUPPLEMENTING ARTICLE 6 OF THE ORDINANCE ON ROYALTIES

THE GOVERNMENT

Pursuant to the December 25, 2001 Law on Organization of the Government;

Pursuant to the April 10, 1998 Ordinance on Royalties;

Pursuant to the November 22, 2008 Ordinance Amending and Supplementing Article 6 of the Ordinance on Royalties;

At the proposal of the Minister of Finance,

DECREES:

Chapter I

ROYALTY PAYERS AND ROYALTY-LIABLE OBJECTS

Article 1. Organizations and individuals that exploit natural resources in any forms shall pay royalties under Article 1 of the Ordinance on Royalties.

Article 2. Natural resources in the mainland, islands, internal waters, territorial seas, the exclusive economic zone and continental shelf under the sovereignty and jurisdiction of the Socialist Republic of Vietnam are liable to royalties, including:

1. Metallic minerals.

2. Non-metallic minerals, including also

minerals used as ordinary construction materials and soil exploited for ground leveling, construction and embankment or use as raw materials or for other purposes; natural mineral water and thermal water specified in the Law on Minerals.

3. Petroleum oil being crude oil specified in Clause 2, Article 3 of the Petroleum Law.

4. Fuel gas being natural gas specified in Clause 3, Article 3 of the Petroleum Law.

5. Coal gas specified in Clause 3, Article 1 of the Law Amending and Supplementing a Number of Articles of the Petroleum Law.

6. Natural forest products, covering plants and animals of all kinds and other products.

7. Natural aquatic resources, covering wild animals and plants in the sea, rivers, streams and lakes.

8. Natural water, covering surface water and ground water, excluding natural mineral water and thermal water specified in Clause 2 of this Article.

9. Other natural resources.

Article 3. For natural resource-exploiting enterprises established under joint venture or business cooperation contracts, royalties payable by joint-venture enterprises or foreign partners shall be indicated in business cooperation contracts and included in the volumes of products shared to Vietnamese partners. When sharing exploited products, Vietnamese partners shall remit royalties into the state budget in accordance with the State Budget Law and this Decree.

Chapter 2

ROYALTY BASES, TARIFF AND PAYMENT METHODS

Article 4. Royalty bases include the actually exploited output of commodity natural resources.

royally-liable price and tax rate. Particularly for crude oil, natural gas and coal gas (below collectively referred to as oil and gas), royalty bases shall be determined on the basis of the progressive part of the total actually extracted output of oil or gas in each tax period, calculated on the basis of the average daily output of extracted oil or gas under an oil or gas contract, royalty rate and number of extraction days in a tax period.

Article 5. The actually exploited output of commodity natural resources is the quantity, weight or volume of natural resources actually exploited in a tax period, regardless of the purposes of exploitation.

Article 6.

1. Royalty-liable price is the selling price of a natural resource product unit at the place of exploitation.

a/ For natural resources exploited in a month which are of the same grade and quality and then, part of their output is sold at the place of exploitation at the market price while the remainder is sold to other places or put into production, processing, sorting, classification or selection, the royalty-liable price of the whole output of exploited natural resources is the value-added tax-exclusive selling price of such natural resource product unit at the place of exploitation;

b/ If in a month, there is an exploited output of natural resources but no turnover from the sale thereof, the royalty-liable price of a natural resource unit shall be determined based on the royalty-liable price of the natural resource product unit in the preceding month.

2. When the selling price of a natural resource product unit cannot be determined under Clause 1 of this Article, the royalty-liable price of a natural resource unit shall be determined based on one of the following grounds:

a/ The average market selling price of an exploited natural resource unit of the same category and equivalent value;

b/ The selling price of a refined product unit and the content of this substance in the exploited natural resource, or the price of a refined product and the content of each substance in the exploited natural resource;

c/ The percentage of the selling price of a product manufactured and processed from the exploited natural resource.

3. Royalty-liable price in some specific cases is stipulated as follows:

a/ For natural water used for hydropower generation, it is the average selling price of commodity electricity; for mineral water and natural water used for other purposes, it is prescribed at Point c. Clause 2 of this Article;

b/ For timber, it is the selling price at the place of delivery;

c/ For oil and gas. it shall be determined as follows:

For crude oil. it is the weighted average price of crude oil sold at the place of delivery and receipt under an arm's length trading contract.

For natural gas and coal gas. it is the selling price indicated in an arm's length trading contract at the place of delivery and receipt.

The Ministry of Finance shall specify royalty-liable prices of crude oil, natural gas and coal gas which are sold not under an arm's length trading contract.

4. The Ministry of Finance shall guide the determination of royalty-liable prices mentioned in this Article.

5. Provincial-level People's Committees shall specify royalty-liable prices of natural resources of which product unit selling prices cannot yet be determined (except oil. gas and natural water used for hydropower generation) under the Finance Ministry's guidance.

Article 7.

1. The royalty tariff is specified in Appendices I and II to this Decree.

2. Based on the market price of and management requirements for each category of natural resource in each period, the Ministry of Finance shall assume the prime responsibility for, and coordinate with concerned ministries and branches in. submitting to the Prime Minister for decision the adjustment of royalty rates for each category of natural resource in the royalty tariff enclosed with this Decree in line with the tariff specified in Article 1 of the November 22, 2008 Ordinance Amending and Supplementing Article 6 of the Ordinance on Royalties.

Article 8. Natural resource exploiters shall register, declare and pay royalties in accordance with the tax administration law. Particularly for oil and gas, royalty registration, declaration and payment are specified as follows:

1. Royalties for oil and gas extraction shall be paid in crude oil. natural gas or coal gas, in cash, or partially in cash and partially in crude oil, natural gas or coal gas as prescribed by the Ministry of Finance. Tax agencies shall notify in writing 6 months in advance taxpayers of the royalty payment method.

2. Royalties in crude oil. natural gas or coal gas shall be paid at the place of delivery and receipt. When tax agencies request the payment of royalties at other places, royalty payers may include in payable royalty amounts freights and other direct expenses arising as a result of change of places for tax payment.

Chapter III

ROYALTY EXEMPTION AND REDUCTION

Article 9. Royalties may be exempted or reduced in the following cases:

1. Natural resource exploiters that encounter natural disasters, enemy sabotage or unexpected accidents, causing losses to natural resources for which royalties have been declared and paid, will be considered for exemption from payable royalties for the lost volumes of natural resources. The paid royalty amount may be refunded or cleared against the subsequent period's payable royalty amount.

2. Exploiters of offshore aquatic resources by high-capacity vessels are exempt from royalty payment for 5 years after they are granted exploitation licenses, and entitled to a 50% royalty reduction for 5 subsequent years. Past the above tax exemption or reduction duration, if still suffering losses, they will be further considered for reduction of royalty amounts corresponding to losses arising in each year for not more than 5 subsequent consecutive years.

3. Royalties will be exempted for natural forest products which individuals are licensed to exploit, such as timber, tree branches, firewood, bamboo of all kinds and thatch, for their daily-life needs.

4. Royalties will be exempted for natural water used for generation of hydropower not fed into the national power grid.

5. Exploiters of soil for the following purposes will be exempted from royalties:

a/ Ground leveling for construction of security and defense works;

b/ Ground leveling for construction of dikes and irrigation works for agricultural, forestry and fishery purposes;

c/ Ground leveling for construction of humanitarian or charity works or works for people with meritorious services to the revolution; soil exploited and used on allocated or leased areas;

d/ Ground leveling for construction of mountainous infrastructure works (mountainous districts) for local socio-economic development;

e/ Ground leveling for construction of national key works under the Government's decisions on a case-by-case basis.

Royalty exemption mentioned in Clause 5 of this Article is applicable only to exploiters of natural resources for non-commercial purposes.

Article 10. Royalty exemption until 2010 for marine resource exploiters and unprocessed salt makers is specified in Clause 2, Section II of the National Assembly's Resolution No. 47/2005/ QH11 of November 1, 2005.

Chapter IV

IMPLEMENTATION PROVISIONS

Article 11. This Decree takes effect on the date of its signing.

1. To annul the Government's Decrees No. 68/ 1998/ND-CP of September 3,1998. and No. 147/2006/ND-CP of December 1, 2006, detailing the implementation of the Ordinance on Royalties, and Articles 44 thru 47 of the Government's Decree No. 48/2000/ND-CP of September 12, 2000, detailing the implementation of the Petroleum Law.

2. For investment projects or oil and gas contracts signed before the effective date of this Decree, and royalty payment is indicated in investment licenses or oil and gas contracts, the provisions of those investment licenses or signed oil and gas contracts apply. For oil and gas contracts not yet signed before the effective date of this Decree while specific royalty rates have been approved by the Prime Minister, the Prime Minister's approval decisions shall be complied with.

Article 12. The Ministry of Finance shall guide the implementation of this Decree.

Ministers, heads of ministerial-level agencies, heads of government-attached agencies, presidents of provincial-level People's Committees, and concerned organizations and individuals shall implement this Decree.-

| ON BEHALF OF THE GOVERNMENT |

APPENDIX I

ROYALTY TARIFF (EXCLUDING CRUDE OIL, NATURAL GAS AND COAL GAS)

(To the Government's Decree No. 05/2009/ND-CP of January 19, 2009)

No. | Group or category of natural resource | Royalty rate (%) | ||

I | METALLIC MINERALS |

| ||

1 | Minerals of ferrous metals (iron, manganese, titanium, etc.) | 7 | ||

2 | Minerals of non-ferrous metals: |

| ||

2.1 | Spread gold ores | 9 | ||

2.2 | Gold nuggets | 9 | ||

2.3 | Rare earths | 12 | ||

2.4 | Platinum, tin, tungsten, silver and antimony | 7 | ||

2.5 | Lead, zinc, aluminum, bauxite, copper, nickel, cobalt, molybdenum, mercury, magnesium, vanadium and platinum | 7 | ||

2.6 | Other minerals of non-ferrous metals | 7 | ||

II | NON-METALLIC MINERALS (excluding natural thermal water and mineral water specified in Section V below) |

| ||

1 | Non-metallic minerals used as ordinary construction materials: |

| ||

1.1 | Soil exploited for ground leveling and embankment | 3 | ||

1.2 | Other non-metallic minerals used as ordinary construction materials (rock, sand, gravel, soil for brick-making, etc.) | 5 | ||

2 | Non-metallic minerals used as high-grade construction materials (granite, dolomite, fireclay, quartzite, etc.) | 7 | ||

3 | Non-metallic minerals used in industrial production (pyrite, phosphorite, kaolin, mica, technical quartz, limestone, cement, and sand for glass-making, etc.) | 7 | ||

| Particularly: apatite and serpentine | 3 | ||

4 | Coal: |

| ||

4.1 | Pit anthracite coal | 4 | ||

4.2 | Open-cast anthracite coal | 6 | ||

4.3 | Lignite and fat coal | 6 | ||

4.4 | Other coals | 4 | ||

5 | Gemstones: |

| ||

5.1 | Diamond, ruby, sapphire, emerald, alexandrite and black precious opal | 16 | ||

5.2 | Adrite, rodolite, pyrope, berine, spinel, topaz, crystalline quartz (bluish-purple, greenish-yellow or orange), chrysolite, precious opal (white or scarlet), feldspar, birusa and nephrite | 12 | ||

5.3 | Other gemstones | 10 | ||

6 | Other non-metallic minerals | 4 | ||

III | NATURAL FOREST PRODUCTS |

| ||

1 | Log timber of all kinds: |

| ||

1.1 | Group I | 40 | ||

1.2 | Group II | 35 | ||

1.3 | Groups III and IV | 30 | ||

1.4 | Groups V, VI, VII and VIII | 25^ | ||

2 | Pit props | 20 | ||

3 | Wood used as raw materials for paper production (snowbell, pine, etc.) | 20 | ||

4 | Wood used as masts or bottom stakes | 20 | ||

5 | Impregnated wood, mangrove wood and cajuput wood | 20 | ||

6 | Tree branches and tops | 15 | ||

7 | Firewood | 5 | ||

8 | Bamboo of all kinds | 10 | ||

9 | Materia medica: |

| ||

9.1 | Sandalwood, calambac | 25 | ||

9.2 | Anise, cinnamon, cardamom and liquorice | 10 | ||

9.3 | Other materia medica | 5 | ||

10 | Other natural forest products: |

| ||

10.1 | Forest birds and animals (those allowed to be exploited) | 20 | ||

10.2 | Other natural forest products | 5 | ||

IV | NATURAL AQUATIC RESOURCES |

| ||

1 | Pearl, abalone and sea-cucumber | 10 | ||

2 | Shrimp, fish, cuttlefish and other aquatic resources | 2 | ||

V | NATURAL MINERAL WATER AND NATURAL WATER |

| ||

1 | Natural mineral water; purified natural water, bottled or canned | 8 | ||

2 | Natural water used for hydropower generation | 2 | ||

3 | Natural water exploited for production branches (other those specified at Points 1 and 2): |

| ||

3.1 | Used as main or auxiliary materials to constitute material elements in manufactured products | 3 | ||

3.2 | Used for production (industrial sanitation, cooling, steaming, etc.) |

| ||

a | Use of surface water | 1 | ||

b | Use of ground water | 2 | ||

3.3 | Natural water used for clean water production or for agriculture, forestry, fishery and salt making, and natural water exploited from dug or bored wells for daily-life needs | 0 | ||

| - Use of ground water for clean water production | 0.5 | ||

4 | Natural water exploited for purposes other than those specified at Points 1, 2 and 3 |

| ||

4.1. | For services: |

| ||

a | Use of surface water | 3 | ||

b | Use of ground water | 5 | ||

4.2 | For industrial production, construction and mining: |

| ||

a | Use of surface water | 3 | ||

b | Use of ground water | 4 | ||

4.3 | For other purposes: |

| ||

a | Use of surface water | 0 | ||

b | Use of ground water | 0.5 | ||

VI | OTHER NATURAL RESOURCES | 10 | ||

1 | Swallow's nests | 20 | ||

2 | Other natural resources | 10 | ||

APPENDIX II

ROYALTY TARIFF FOR CRUDE OIL, NATURAL GAS AND COAL GAS

(To the Government's Decree No. 05/2009/ND-CP of January 19, 2009)

No. | Output | Projects eligible for investment promotion (%) | Other projects (%) |

I | FOR CRUDE OIL |

|

|

1 | Up to 20,000 barrels/day | 6 | 8 |

2 | Between over 20.000 and 50,000 barrels/day | 8 | 10 |

3 | Between over 50,000 and 75,000 barrels/day | 10 | 12 |

4 | Between over 75,000 and 100,000 barrels/day | 12 | 17 |

5 | Between over 100,000 and 150,000 barrels/day | 17 | 22 |

6 | Over 150,000 barrels/day | 22 | 27 |

II | FOR NATURAL GAS AND COAL GAS |

|

|

1 | Up to 5 million m3/day | 0 | 0 |

2 | Between over 5 million and 10 million m3/day | 3 | 5 |

3 | Over 10 million m3/day | 6 | 10 |