Nội dung toàn văn Circular No. 41/2006/TT-BTC of May 12, 2006, guiding the implementation of The Prime Minister’s Decision No. 161/2005/QD-TTg of June 30, 2005, on expanding the pilot self-assessment and self-payment of house and land tax, income tax on high-income earners and license tax by production and business establishments.

THE MINISTRY OF FINANCE | SOCIALIST REPUBLIC OF VIET NAM |

No. 41/2006/TT-BTC | Hanoi, May 12, 2006 |

CIRCULAR

GUIDING THE IMPLEMENTATION OF THE PRIME MINISTER’S DECISION No. 161/2005/QD-TTg OF JUNE 30, 2005, ON EXPANDING THE PILOT SELF-ASSESSMENT AND SELF-PAYMENT OF HOUSE AND LAND TAX, INCOME TAX ON HIGH-INCOME EARNERS AND LICENSE TAX BY PRODUCTION AND BUSINESS ESTABLISHMENTS

Pursuant to the 1992 Ordinance on House and Land Tax, the 1994 Ordinance Amending and Supplementing a Number of Articles of the Ordinance on House and Land Tax and the Government’s Decree No. 94/CP of August 25, 1994, detailing the implementation of the Ordinance on House and Land Tax and the Ordinance Amending and Supplementing a Number of Articles of the Ordinance on House and Land Tax;

Pursuant to May 19, 2001 Ordinance No. 35/2001/PL-UBTVQH10 on Income Tax on High-Income Earners, March 24, 2004 Ordinance Amending and Supplementing a Number of Articles of the Ordinance on Income Tax on High-Income Earners, and the Government’s Decree No. 147/2004/ND-CP of July 23, 2004, detailing the implementation of the Ordinance on Income Tax on High-Income Earners;

Pursuant to the Government’s Decree No. 75/2002/ND-CP of August 30, 2002, on adjusting license tax rates;

Pursuant to the Prime Minister’s Decision No. 197/2003/QD-TTg of September 23, 2003, on the pilot implementation of the mechanism of tax self-assessment and self-payment by production and business establishments;

Pursuant to the Prime Minister’s Decision No. 161/2005/QD-TTg of June 30, 2005, on expanding the pilot self-assessment and self-payment of special consumption tax at the stage of domestic production; natural resource tax; house and land tax; income tax on high-income earners; and license tax by production and business establishments;

The Ministry of Finance hereby guides the implementation as follows:

I. SUBJECTS OF APPLICATION:

Taxpayers governed by Decision No. 161/2005/QD-TTg as guided in this Circular are production, business and service establishments (hereinafter collectively referred to as business establishments) which are specified in Clause 2, Article 1 of the Prime Minister’s Decision No. 197/2003/QD-TTg of September 23, 2003, and guiding documents issued by the Ministry of Finance.

II. TAX REGISTRATION:

Business establishments implementing on a pilot basis the mechanism of self-assessment and self-payment of house and land tax, income tax on high-income earners and license tax shall continue using their tax identification numbers already granted by tax offices, without having to re-register their tax identification numbers with tax offices.

III. TAX DECLARATION AND PAYMENT:

1. House and land tax:

1.1. Declaration of house and land tax:

Business establishments shall declare house and land tax according to a declaration form issued together with this Circular (form No. 01-06/TND, not printed herein) and submit their declaration forms no later than January 31 every year (calendar year) to the Sub-Department of Tax of the locality where the land liable to house and land tax is located. Some items in the house and land tax declaration form are explained as follows:

a/ Land area liable to house and land tax is the whole land area liable to house and land tax actually managed and used by the business establishment (including land areas currently used by other organizations and individuals).

In case business establishments have been granted land-use right certificates or land assignment decisions by competent state agencies for their land areas, land areas liable to house and land tax are the whole land areas liable to house and land tax written in such land-use right certificates or land assignment decisions. If business establishments have not yet been granted land-use right certificates or land assignment decisions for their land areas, they shall declare those land areas actually in use.

b/ The land grade used for the determination of the number by which agricultural land use tax will be multiplied to calculate the house and land tax shall follow the guidance in Clauses 1, 2 and 3, Section II of the Finance Ministry’s Circular No. 83-TC/TCT of October 7, 1994, guiding the implementation of the Government’s Decree No. 94/CP of August 25, 1994, detailing the implementation of the Ordinance on House and Land Tax (or be notified by the tax office in case the business establishments fail to determine such number).

c/ The paddy price used for the calculation of house and land tax shall be that used for the calculation of agricultural land use tax in the year-end crop of the year preceding the year of collection of house and land tax as announced by provincial/municipal People’s Committees.

1.2. Payment of house and land tax:

Production and business establishments shall pay house and land tax into the state budget according to the declared tax amounts.

House and land tax shall be paid twice a year, half of the total payable tax amount each time. The first payment shall be made no later than April 30 while the second payment no later than October 31 every year. If taxpayers wish to pay the whole payable house and land tax amount once, they shall pay it according to the deadline for the first payment.

Upon remittance of the tax money into the state budget, business establishments shall use the paper for state budget remittance (by account transfer or in cash) and completely fill in the paper as instructed in the Finance Ministry’s Circular No. 80/2003/TT-BTC of August 13, 2003, guiding the concentration and management of state budget revenues through state treasuries.

In case a business establishment pays both the payable tax amount and fine arising in the current period and the tax amount and fine owed from a previous period which is, however, not specified, the tax office shall offset them first against the tax amount and fine still owed from the previous period, then against the tax amount and fine payable in the current period.

House and land tax shall be paid by business establishment to the state treasuries of districts where the taxable land is located and be recorded according to regulations on the budget index.

If a business establishment undergoes merger, consolidation, separation, split-up, dissolution, bankruptcy, ownership transformation, relocation to another province or city, state enterprise assignment, sale, contracting or lease, it shall have to remit all house and land tax arrears into the state budget before such change. If a business establishment has any overpaid house and land tax amount, the tax office shall refund it such amount according to current regulations.

2. Income tax on high-income earners (called personal income tax for short):

The declaration, payment and finalization of personal income tax shall comply with the provisions of the Ordinance on Income Tax on High-Income Earners and guiding documents currently in force.

2.1. Declaration of personal income tax:

For regular incomes being salaries and wages paid under labor contracts, business establishments shall withhold, declare and temporarily pay personal income tax on a monthly basis. Business establishments implementing the mechanism of self-assessment and self-payment on a pilot basis shall make full and accurate declaration according to form No. 03a/TNTX, issued together with this Circular (not printed herein). If the tax amount withheld each month is less than VND 5 million, declaration can be made in form No. 03a/TNTX on a quarterly basis but the tax money is still withheld every month. Whether or not tax declaration can be made on a quarterly basis shall be determined every year, depending on the total income tax amount withheld in the first month of the year.

Tax declaration forms shall be submitted to tax offices no later than the 25th of the month following the month of arising incomes. The deadline for submission of quarterly tax declaration forms is the 25th of the first month of the subsequent quarter.

In case a business establishment makes incomplete or improper declaration according to the set form or fails to certify the legal validity of the declaration (signature and stamp), it shall be regarded as not having submitted the declaration to the tax office.

Business establishments shall take responsibility before law for the truthfulness and accuracy of their monthly and quarterly personal income tax declaration (if any). If the tax office detects through inspection any untruthful and inaccurate data, it shall impose penalties according to the provisions of law.

2.2. Payment of personal income tax:

Monthly, business establishments shall remit personal income tax into the state budget according to the declared tax amounts. The deadline for personal income tax payment is the 25th of the month following the month of arising tax amounts. In case of quarterly payment, the deadline is the 25th of the first month of the subsequent quarter. For business establishments paying personal income tax by account transfer through a bank or credit institution, the day of remittance into the state budget shall be identified as the date such bank or credit institution deducts and transfers money to the state treasury according to the papers of state budget remittance issued by business establishments; for business establishments paying personal income tax in cash, the date of remittance into the state budget shall be the date the treasury or tax office receives the tax money.

Business establishments shall completely fill in the paper of remittance as instructed by the tax office and state treasury office. On such paper, business establishments shall indicate the personal income tax amount and related fine (if any) payable in each tax period. In case a business establishment fails to indicate the period for which the tax amount and fine are paid, the tax office shall offset them first against the tax amount and fine still owed then against the tax amount and fine payable in the period.

If a business establishment undergoes transformation of type of enterprise and form of ownership such as merger, consolidation, separation, split-up, dissolution, bankruptcy, ownership transformation, relocation to another province or city, state enterprise assignment, sale, contracting or lease, it shall have to declare the tax amount arising by the time of merger, consolidation, separation, split-up, dissolution, bankruptcy, ownership transformation, relocation to another province or city, state enterprise assignment, sale, contracting or lease (also declaring adjustments to previous periods’ erroneous data, if detected). It shall submit the tax declaration and remit all personal income tax arrears into the state budget within 30 days after the date of issuance of the decision on merger, consolidation, separation, split, dissolution, bankruptcy, ownership transformation, relocation to another province or city, state enterprise assignment, sale, contracting or lease. If a business establishment has any overpaid or insufficiently withheld personal income tax amount, the tax office shall refund it such amount according to current regulations.

2.3. Replacement of personal income tax declaration forms and receipts:

- Form No. 03a/TNTX and form No. 10/TNTX issued together with the Finance Ministry’s Circular No. 12/2005/TT-BTC of February 4, 2005, are replaced with form No. 03a/TNTX and form No. 10/TNTX issued together with this Circular (not printed herein).

- Form No. 08/TNTX issued together with the Finance Ministry’s Circular No. 12/2005/TT-BTC of February 4, 2005, is replaced with form No. 08a/TNTX and form No. 08b/TNTX issued together with this Circular (not printed herein), including:

+ Form No. 08a/TNTX is a simple form applicable to individuals having taxable incomes in Vietnam only, excluding professional singers, circus artists, dancers, football players, athletes.

+ Form No. 08b/TNTX is a complicated form applicable to foreign and Vietnamese individuals having taxable incomes in Vietnam and abroad, and professional singers, circus artists, dancers, football players, athletes.

- Personal income tax receipts:

Form CTT 10B (income tax receipt) issued together with the Finance Ministry’s Circular No. 81/2004/TT-BTC of August 13, 2004, is replaced with form CTT 10B (income tax receipt) issued together with this Circular (not printed herein).

Modified income tax declaration forms and receipts mentioned herein shall also apply to individuals and taxpayers not implementing the mechanism of tax self-assessment and self-payment on a pilot basis.

3. License tax:

3.1. License tax rates:

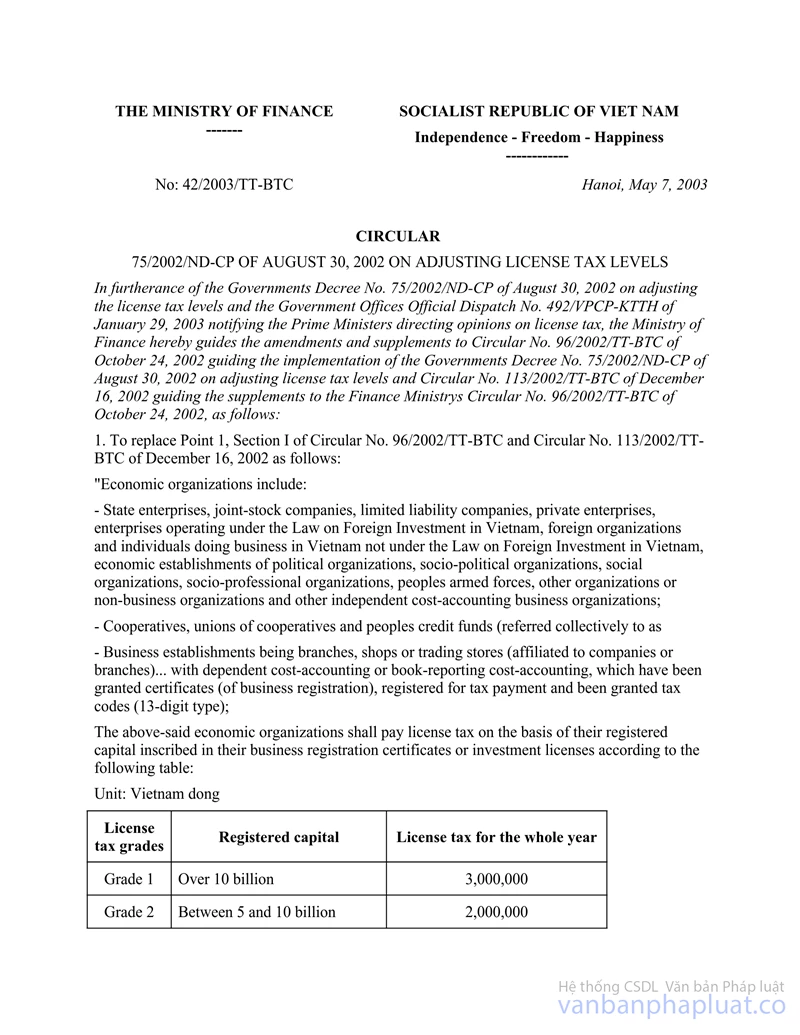

Business establishments implementing the mechanism of tax self-assessment and self-payment on a pilot basis shall determine by themselves license tax rates under the guidance at Points 1 and 2 of the Finance Ministry’s Circular No. 42/2003/TT-BTC of May 7, 2003, guiding supplements and amendments to the Finance Ministry’s Circular No. 96/2002/TT-BTC of October 24, 2002, guiding the implementation of the Government’s Decree No. 75/2002/ND-CP of August 30, 2002, on adjusting license tax rates.

3.2. Declaration and payment of license tax:

Business establishments shall make self-assessment and submit their declarations made according to forms No. 04-06/MB issued together with this Circular (not printed herein), and pay by themselves license tax into the state budget.

For business establishments that have branches, factories, manufacture workshops, shops, places of service provision, etc., practicing dependent cost-accounting and located in the same locality (province or centrally run city), they (head offices) shall declare and pay license tax for their head offices and such branches, factories, manufacture workshops, shops, places of service provision. Those branches, factories, manufacture workshops, shops, places of service provision, etc., which practice dependent cost-accounting and located in other localities (provinces or centrally-run cities) shall declare and pay license tax in such localities.

The time of declaration and payment of license tax for each specific case is as follows:

3.2.1. For operating business establishments:

a/ Declaration and submission of license tax declaration forms:

Business establishments shall declare license tax according to forms No. 04-06/MB issued together with this Circular (not printed herein) and submit such declaration forms annually.

The deadline for submission of license tax declaration forms to managing tax offices is January 31 of the calendar year. Bases for the determination of license tax rates and levels are stated in Section 3.1 of Section III above.

b/ Payment of license tax:

Business establishments shall remit license tax into the state budget according to the tax amounts already declared to tax offices no later than January 31 of the calendar year.

Business establishments shall completely fill in all items on the paper of remittance as instructed by the tax office and treasury office. If business establishments pay license tax by account transfer through a bank or credit institution, the date of remittance of tax money into the state budget shall be identified as the date the bank or credit institution deducts and transfers the tax money to the state treasury; if business establishments pay license tax in cash, the date of remittance of tax money into the state budget shall be identified as the date the treasury office or tax office receives the tax money.

3.2.2. For newly established business establishments:

After being established and granted the business registration certificates, business establishments shall fill in license tax declaration forms, submit them and pay license tax within 30 days after the date they are granted the tax registration certificates (tax identification numbers). For business establishments set up and granted the tax registration certificates during the first half of a year, they shall pay license tax for the whole year. For business establishments set up and granted the tax registration certificates during the second half of a year, they shall pay 50% of license tax for the whole year.

If an operating business establishment sets up other dependent cost-accounting business units in the same locality (province or centrally run city), it (head office) shall declare and pay additional license tax for such dependent units according to the time limit and ways of determination of payable license tax amounts applicable to newly set-up establishments mentioned above.

4. Declaration of adjustments to house and land tax, personal income tax, license tax:

4.1. For house and land tax and personal income tax:

After submitting declaration forms to the tax office, if business establishments find any mistakes in the declared data (detected by business establishments themselves or notified by the tax office), they shall declare adjustments to the tax office as follows:

- If the time limit for declaration has not yet expired, business establishments shall fill in and submit new declaration forms in replacement of the ones already submitted to the tax office. In these new declaration forms, business establishments must indicate the date of submission of the substituted declaration forms to the tax office.

- If the time limit for declaration has expired, business establishments shall be only allowed to declare adjustments to mistakenly declared data on the declaration forms already submitted to the tax office. Once the tax office has issued decisions on inspection of tax finalization, no adjustment shall be accepted.

4.2. For license tax:

- Within five years counting from the date of submission of license tax declaration forms to the tax office, if finding any mistakes in the declared data (detected by business establishments themselves or notified by the tax office) or setting up new branches, shops, etc., in the same locality, business establishments shall declare adjustments to replace the declaration forms already submitted to the tax office. In the adjustment declaration forms, business establishments must indicate the date of submission of the substituted declaration forms, the increased or reduced tax amounts and the reason therefor.

- In case a business establishment has paid the license tax money to the tax office and the adjustment gives rise to a tax difference, it shall have to pay the license tax arrears, if such tax difference is positive or to make deductions from the following year’s payable license tax amount, if such tax difference is negative.

- In case the tax office has issued decisions on inspection of tax finalization, no adjustment shall be accepted.

IV. TASKS, POWERS AND RESPONSIBILITIES OF TAX OFFICES:

Apart from the tasks, powers and responsibilities of tax offices defined in legal documents on house and land tax and related documents, tax offices which manage production and business establishments implementing the mechanism of self-assessment and self-payment of house and land tax, personal income tax and license tax shall be responsible for:

1. Disseminating and popularizing among business establishments and responding to their inquiries on tax policies and self-assessment and self-payment procedures so that business establishments understand and comply with the provisions of law on taxes and the tax self-assessment and self-payment mechanism.

2. Monitoring business establishments in performing tax self-assessment and self-payment obligations:

- If beyond the deadline for submission of declaration forms business establishments still fail to send their declaration forms to tax offices according to regulations, tax offices shall send notices reminding the submission of tax declaration forms and impose administrative sanctions according to current regulations. In case a business establishment still fails to submit the declaration form after receiving the tax notice and being administratively sanctioned, the tax office shall fix a tax amount for temporary payment according to the provisions of law on house and land tax, personal income tax and license tax.

- Beyond the prescribed tax payment deadline, tax offices shall send notices reminding business establishments to pay tax and impose fines for late payment of tax amounts still owed to the state budget according to regulations.

3. Supervising and inspecting regularly or irregularly production and business establishments in their implementation of the mechanism of self-assessment and self-payment of house and land tax, personal income tax and license tax.

4. Applying measures to force business establishments to pay tax arrears and fines according to the provisions of law.

5. Keeping confidential supplied information on production and business establishments according to regulations.

V. ORGANIZATION OF IMPLEMENTATION:

1. This Circular takes effect 15 days after its publication in “CONG BAO”. Other matters not guided in this Circular shall still comply with the guidance in the Finance Ministry’s Circular No. 83-TC/TCT of October 7, 1994, and Circular No. 71/2002/TT-BTC of August 19, 2002, guiding the implementation of the Government’s Decree No. 94/CP of August 25, 1994, detailing the implementation of the Ordinance on House and Land Tax, the Finance Ministry’s Circular No. 81/2004/TT-BTC of August 13, 2004, and Circular No. 12/2005/TT-BTC of February 4, 2005, guiding the implementation of the Government’s Decree No. 147/2004/ND-CP of July 23, 2004, detailing the implementation of the Ordinance on Income Tax on High-Income Earners, and current regulations on license tax.

2. The General Department of Taxation shall be responsible for organizing the pilot implementation of the mechanism of self-assessment and self-payment of house and land tax, personal income tax and license tax by production and business establishments according to the provisions of this Circular.

3. In the course of implementation, if facing any problems, branches, localities and production and business establishments should promptly report them to the Ministry of Finance for study and additional guidance.

| FOR THE MINISTER OF FINANCE |