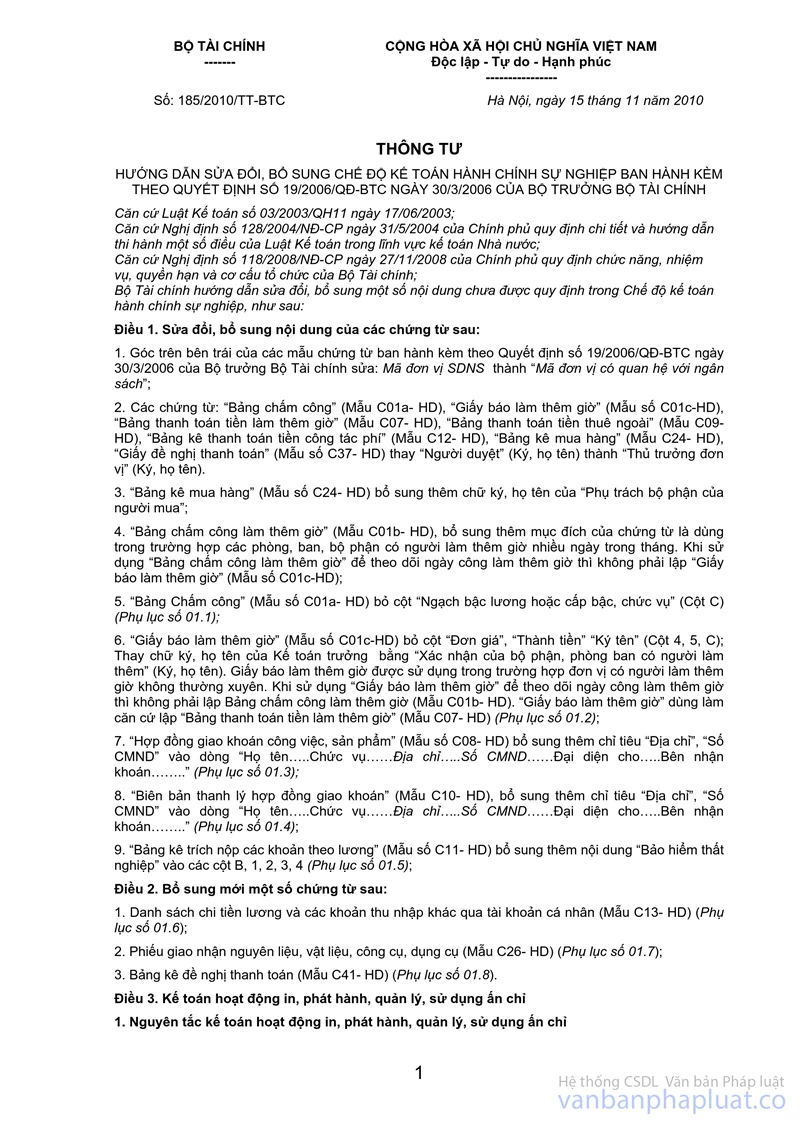

Circular 185/2010/TT-BTC amending supplementing the public-sector administrative accounting đã được thay thế bởi Circular 107/2017/TT-BTC on guidelines for public sector accounting và được áp dụng kể từ ngày 24/11/2017.

Nội dung toàn văn Circular 185/2010/TT-BTC amending supplementing the public-sector administrative accounting

THE MINISTRY OF FINANCE | THE SOCIALIST REPUBLIC OF VIETNAM |

No. 185/2010/TT-BTC | Hanoi, November 15, 2010 |

CIRCULAR

PROVIDING GUIDANCE ON AMENDING AND SUPPLEMENTING THE PUBLIC-SECTOR ADMINISTRATIVE ACCOUNTING REGULATIONS ISSUED UNDER THE DECISION NO. 19/2006/QD-BTC OF THE MINISTER OF FINANCE DATED MARCH 30, 2006

Pursuant to the Law on Accounting No. 03/2003/QH11 dated June 17, 2003;

Pursuant to the Decree No.128/2004/ND-CP dated May 31, 2004 of the Government on specifying and providing guidance on the implementation of a number of articles of the Law on Accounting in the Government accounting;

Pursuant to Decree No. 118/2008/ND-CP dated November 27, 2008 of the Government on defining the functions, tasks, powers and organizational structure of the Ministry of Finance;

The Ministry of Finance hereby provides guidance on amending and supplementing several contents which have not been included in the public sector accounting regulations as follows:

Article 1. Amending and supplementing existing contents of the following accounting documents:

1. At the upper left corner of the specimen of the accounting voucher appended to the Decision No. 19/2006/QD-BTC of the Minister of Finance dated March 30, 2006, the field Code of the unit using the state budget is replaced by Code of the unit affiliated with the State Budget;

2. The field Approved by (Signature and full name) in the bottom section of documents, such as “timesheet” (Form No. C01a- HD), “Overtime work note” (Form No. C01c-HD), “Overtime pay sheet” (Form No. C07- HD), “Outsourced service payment sheet” (Form No. C09- HD), “Business travel expense payment statement” (Form No. C12- HD), “List of procured goods" (Form No. C24- HD), and “Payment request note” (Form No. C37- HD), is replaced by The unit’s Head (Signature and full name).

3. “List of procured goods” (Form No. C24- HD) is supplemented with signature and full name of Officer in charge of procurement department;

4. “Overtime sheet” (Form No. C01b- HD) is supplemented with its purpose stating that this document is applied to departments or sub-departments whose employees work overtime in multiple days of a month. Where the said form “Overtime sheet” is used for the purpose of keeping track of days of overtime work, preparation of “Overtime work note” (Form No. C01c-HD) is not necessary;

5. The column Salary scale, level or professional rank or title (Column C) is deleted from “Timesheet” (Form No. C01a- HD) (in the Appendix No. 01.1);

6. In the "Overtime work note” (Form No. C01c-HD), columns such as Unit price, Total sum and Signed by (Column 4, 5, C) are deleted; and the field signature and full time of the Chief Accountant is replaced by Confirmed by the department or division in charge of employee working overtime” (Signature, full name). Overtime work note is applied to any unit whose employees work overtime in an irregular manner. Where the said form “Overtime work note” is used for the purpose of keeping track of days of overtime work, preparation of “Overtime sheet” (Form No. C01b-HD) is not necessary. “Overtime work note” is used as the basis for preparing “Overtime pay sheet” (Form No. C07- HD) (in the Appendix No. 01.2);

7. The field Address, ID card number is inserted into the existing line to become Full name…..Title…..Address…..ID card number…..Acting as the representative of.....Contractor…..in the “Lump sum contract for completed work or product” (Form No. C08- HD) (in the Appendix No. 01.3);

8. The field Address, ID card number is inserted into the existing line to become Full name…..Title…..Address…..ID card number…..Acting as the representative of.....Contractor…..in the “Record of lump sum contract termination” (Form No. C10- HD) (in the Appendix No. 01.4);

9. The field Unemployment insurance is inserted into column B, 1, 2, 3, 4 in the “Payroll-related expense or deduction sheet” (Form No. C11- HD) (in the Appendix No. 01.5);

Article 2. Adding several new accounting documents:

1. List of salaries or wages and other incomes paid through personal accounts (Form No. C13- HD) (in the Appendix 01.6);

2. Delivery and receipt note of raw input materials, tools and instruments (Form No. C26- HD) (in the Appendix No. 01.7);

3. Schedule of payment requests (Form No. C41- HD) (in the Appendix No. 01.8).

Article 3. Accounting for regulatory forms printing, publication, management and utilization activities

1. Accounting principles for regulatory forms printing, publication, management and utilization activities

- Receipt and dispatch of regulatory forms are reflected in A/C 152 “Raw input materials” which is used for monitoring in detail 2 types of regulatory forms such as allocated and sold ones:

+ Allocated regulatory forms referring to any form allocated for administration and professional operation purposes in a regulatory unit.

+ Sold regulatory forms referring to any form that a regulatory unit is allowed to legally print and publish for the purpose of selling them to eligible entities stipulated by laws and regulations.

- A regulatory unit must fully comply with regulations on management of receipt and dispatch of regulatory forms. Receiving and dispatching both allocated and sold regulatory forms must conform to stipulated procedures and must be documented by receipt or dispatch notes.

- Entering details of both allocated and sold regulatory forms into accounts must be carried out in both warehouse and accounting department on a concurrent basis. In the warehouse department, warehouse keepers must keep books (or cards) to take control of in, out and balance quantity of specific items or types of allocated and sold regulatory forms; meanwhile, the accounting department must keep books to record in, out and balance quantity and value of itemized regulatory forms of same kind. On a regular (monthly or quarterly) basis, accountants must check with warehouse keepers if in, out and balance quantity of specific items and types of regulatory forms is correct, and in case of any variation, inform the chief accountant and head of such unit on a timely manner to promptly identify reasons and find proper solutions.

- Entering in, out and balance quantity of regulatory forms into accounts must be based on actual prices applied in specific circumstances. The actual price of a regulatory form received by the unit granted permission for printing thereof is the actual rental price of printing service specified on a contract for leasing of printing service between such unit and the printing company. The actual price of a self-printed regulatory form is total cost that such unit has spent on printing and binding these forms.

- Related costs (such as transportation, handling, input material and packaging costs, etc.) shall be directly charged for accounts of costs related to utilization of regulatory forms (class-6 accounts and those for itemization of activities), specifically including:

+ Costs relating to allocated regulatory forms received are charged for Debit A/C 661 (66121);

+ Costs relating to sold regulatory forms dispatched are charged for Debit A/C 631 “Operating expenses";

- Costs, whenever incurred from publication of sold regulatory forms, are charged for Debit A/C 631 “Operating expenses";

- Revenues generated from sale of regulatory forms are entered into A/C 531 “Operating revenues";

- At the end of a given accounting period, accountants must carry forward all publication costs relating to regulatory form sale activities that arise within this period to A/C 531 to determine results of publication of sold regulatory forms;

- At the end of a given accounting period, accountants must measure difference between income and expense account for publication of sold regulatory forms which is brought forward to A/C 421 “Outstanding difference in income and expense”.

2. Accounting method for certain key economic activities

Accounting method for certain key economic activities relating to allocated regulatory forms

- Any cost incurred from leasing of regulatory form design services shall be entered into accounts as follows:

Debit A/C 661 – Operating expenses

Credit A/C 111, 112, 331…

If payments for costs incurred from regulatory form design services are derived from estimated operating expenses, they are simultaneously entered into A/C 008 “Estimated operating expense”.

- Receiving regulatory forms of any kind which are transferred by printing companies as agreed upon in a contract for leasing of printing services between a regulatory unit and printing company shall be entered into accounts as follows:

Debit A/C 152 – Raw input materials (Details of allocated regulatory forms)

Credit A/C 111, 112, 331, 461…

If payment to a printing company is derived from estimated operating expenses, they are simultaneously entered into A/C 008 “Estimated operating expense”.

- Any transportation and handling cost incurred shall be entered into accounts as follows:

Debit A/C 661 – Operating expenses

Credit A/C 111, 112, 331…

- Dispatching regulatory forms for administration and professional operation purposes in a regulatory unit shall be recorded into accounts as follows:

Debit A/C 661 – Operating expense (66121)

Credit A/C 152 – Raw input materials (Details of allocated regulatory forms).

- Delivering regulatory forms to a regulatory unit’s personnel for the purpose of distributing them to external individual and organizational entities shall be posted into accounts as follows:

Debit A/C 312 - Advances

Credit A/C 152 – Raw input materials (Details of allocated regulatory forms).

- Upon receipt of final account statements on the number of regulatory forms dispensed to external individual and organizational entities from receivers of these forms, results of these statements shall be entered into accounts as follows:

Debit A/C 661 – Operating expenses (66121)

Crebit A/C 312 – Advances.

- At year-end, value of in-stock regulatory forms shall be posted into this year’s operating expenses as follows:

Debit A/C 661 – Operating expenses (6612)

Credit A/C 337 – Expenditure already accounted for as carryforward to the next year (3371).

- In the following year, dispatching regulatory forms for administration and professional operation purposes in a regulatory unit (if they are still usable) shall be recorded into accounts as follows:

Debit A/C 337 – Expenditure already accounted for as carryforward to the next year (3371)

Credit A/C 152 – Raw input materials (Details of allocated regulatory forms).

2.2. Accounting method for certain key economic activities relating to sold regulatory forms

- Any cost incurred from leasing of regulatory form design services shall be entered into accounts as follows:

Debit A/C 631 - Manufacturing and trading expenses

Credit A/C 111, 112, 331…

- Receiving regulatory forms of any kind which are transferred by printing companies as agreed upon in a contract for leasing of printing services between a regulatory unit and printing company shall be entered into accounts as follows:

Debit A/C 152 – Raw input materials (Details of sold regulatory forms)

Credit A/C 111, 112

- Costs incurred from publication of sold regulatory forms shall be entered into accounts as follows:

Debit A/C 631 - Manufacturing and trading expenses

Credit A/C 111, 112, 331…

- Delivering regulatory forms to a regulatory unit’s personnel for the purpose of distributing them to external individual and organizational entities shall be posted into accounts as follows:

Debit A/C 312 - Advances

Credit A/C 152 – Raw input materials (Details of sold regulatory forms)

- Upon receipt of final account statements on the number of regulatory forms dispensed to external individual and organizational entities from receivers of these forms, results of these statements shall be entered into accounts as follows:

Debit A/C 531 - Manufacturing and trading income

Credit A/C 312 – Advances.

- Costs recorded as decreases in costs of publication of sold regulatory forms (if any) shall be entered into accounts as follows:

Debit A/C 111, 112, 152…

Credit A/C 631 - Manufacturing and trading expenses.

- Income generated from selling regulatory forms to external individual and organizational entities shall be entered into accounts as follows:

Debit A/C 111, 112 (where cash is immediately collected)

Debit A/C 311 - Receivables (3111) (where cash has not been collected yet)

Credit A/C 531 - Manufacturing and trading income

Credit A/C 333 – Payables to the Government (33311)

(where the regulatory unit pays VAT tax according to the credit-invoice method)

- At the end of an accounting period, carrying forward all costs incurred from publication of regulatory forms of all kinds shall be entered into accounts as follows:

Debit A/C 531 - Manufacturing and trading income

Credit A/C 631 - Manufacturing and trading expenses.

- Stipulated VAT tax payable imposed on publication of regulatory forms (if the regulatory unit pays VAT tax according to the subtraction method) shall be recorded into accounts as follows:

Debit A/C 531 - Manufacturing and trading income

Credit A/C 333 - Payables to the Government.

- At the end of an accounting period, carrying forward difference between income and expense accounts in publication of sold regulatory forms shall be entered into accounts as follows:

+ In case of difference where income account is greater than expense account, such difference is recorded into accounts as follows:

Debit A/C 531 - Manufacturing and trading income

Credit A/C 421 – Outstanding difference between income and expense (4212)

+ In case of difference where expense account is greater than income account, such difference is recorded into accounts as follows:

Debit A/C 421 – Outstanding difference between income and expense (4212)

Credit A/C 531 - Manufacturing and trading income

- The amount of tax payable on corporate income of the regulatory unit generated from publication of sold regulatory forms shall be recorded into accounts as follows:

Debit A/C 421 – Outstanding difference between income and expense (4212)

Credit A/C 333 – Payables to the State Budget (3334)

- Distributing difference where income account is greater than expense in respect of publication of sold regulatory forms in accordance with regulations of the financial system shall be entered into accounts as follows:

Debit A/C 421 – Outstanding difference between income and expense

Credit relevant A/Cs.

Article 4. Accounting for fixed assets

Amending and supplementing the method for determining the historical cost of fixed asset referred to in A/C 211 “Tangible fixed assets” and A/C 213 “Intangible fixed assets” as follows:

1. Tangible fixed assets referred to in A/C 211 “Tangible fixed assets”

- The historical cost of fixed assets created from purchase activities represents the actual purchase price (the price specified on invoice minus (-) trade discounts or price reductions (if any) plus (+) costs incurred from transportation, handling, repair, renovation, improvement, installation and testing activities minus (-) products or scrap materials recovered from the testing stage plus (+) taxes, fees or charges (if any) that a regulatory unit must pay as of the date on which these fixed assets are put into operation;

- The historical cost of fixed assets created from investment and construction activities represents value thereof entered into accounts approved by competent authorities in accordance with regulations on current investment and construction management;

- The historical cost of fixed assets sent from other entities represents value of these assets stated in the record of asset transfer plus (+) costs incurred from transportation, handling, repair, renovation, improvement, installation and testing activities from which products or scrap materials recovered from the testing stage have been subtracted, and then plus (+) taxes, fees or charges (if any) that a regulatory unit must pay as of the date on which these fixed assets are put into operation;

- The historical cost of fixed assets received as gifts or donations represents value of these assets used by financial institutions as the basis for keeping financial accounts or subjected to revaluation by organizations competent to value state-owned assets and approved by financial institutions at the same level plus (+) costs incurred from transportation, handling, repair, renovation, improvement, installation and testing activities from which products or scrap materials recovered from the testing stage have been subtracted, and then plus (+) taxes, fees or charges (if any) that a regulatory unit must pay as of the date on which these fixed assets are put into operation;

- The historical cost of special assets is based on the assumed price for bookkeeping purposes. The assumed price is designated by sector-specific regulatory Ministries and Ministry-level agencies.

2. Intangible fixed assets referred to in A/C 213 “Intangible fixed assets”

- Value of land use rights:

With respect to assigned land for which land use levy is paid, land acquired from disposition of legal land use rights, and/or rented land for which land rental has been paid for the entire rental period, value of land use right shall be calculated, respectively, as the monetary amount payable on that assigned land, sum paid for such disposition, and/or one-off rental payment for such rented land, plus (+) taxes, fees and/or charges (if any).

In case of land assigned without land use levy required, value of land use right shall be determined according to applicable regulations on determination of value of land use right as included in value of assets of organizations assigned such land by the Government plus (+) taxes, fees and/or charges (if any).

- Value of patents is defined as costs paid by a regulatory unit for research and experimental production projects on which the Government has granted patents, or costs incurred by such unit’s repurchase of copyrights on patents from domestic and international researchers.

- Value of authors’ rights, industrial designs and/or utility solutions is defined as total sum paid as royalties to authors and for the Government’s granting of an author's exclusive rights to release and sell their work.

- Value of computer software is defined as total sum paid for hiring of programmers or purchase of computer software for the purpose of implementing a regulatory unit’s programs (applicable to those that need computers for recording and administrative purposes).

With respect to value of gifted or donated computer software, the historical cost is defined as value of assets calculated by financial institutions as the basis for keeping financial accounts or value thereof subjected to revaluation by organizations competent to value state-owned assets and approval by same-level financial institutions.

Article 5. Accounting for remittances to the Government

Account 333 – Payables to the Government is supplemented with one following class-2 account:

- A/C 3335 – Personal income tax: Mirroring personal income tax withheld from taxpayers' income.

Moving contents reflected in “personal income tax” from the account 3337 – Other taxes to the account 3335 – Personal income tax. Method for keeping record of personal income tax in the account 3335 is similar to that in the account 3337.

Supplementing rules of accounting for personal income tax as follows:

- Income payers must declare and pay personal income tax according to the principle of tax deducted at source. Income payers shall be obliged to withhold a sum of money as tax payment remitted into the State Budget before paying income to tax payers;

- Income payers must keep track of details of taxable income of their public officials, servants and other employees, including salaries, wages, bonuses and other earnings, referred to in applicable regulations, as the basis for calculation of the amount of personal income tax payable.

Article 6. Accounting for payables to public servants and employees

Adding contents of payables to employees other than public officials, servants and employees of the regulatory unit to the account 334 ‘Payables to public servants and employees”.

Account 334 is constituted by 2 class-2 accounts as follows:

- A/C 3341 – Payables to public servants and employees: Reflecting payables and status of settlement of payables to public officials, servants and employees of the regulatory unit on salaries and/or payroll-related bonuses, social insurance contributions and other payables included in their income;

A/C 3341 reflects payables to public officials, servants and employees who are those listed as eligible social insurance participants in accordance with applicable regulations enshrined in the laws on social security.

- A/C 3348 – Payables to other employees: Reflecting payables and status of settlement of payables to employees other than the said public officials, servants and employees of the regulatory unit on wages and/or wage-related bonuses (if any) and other payables included in their income;

A/C 3348 reflects payables to other employees who are those not listed as eligible social insurance participants in accordance with applicable regulations enshrined in the laws on social security.

Article 7. Accounting for financing for projects

In A/C 462 – Financing for projects, class-2 accounts thereof shall be reclassified as follows:

- A/C 4621- Financing derived from the State Budget: Reflecting the funding source for projects derived from the State Budget appropriations.

This account is constituted by 2 following class-3 accounts:

+ A/C 46211- Financing for project management: Reflecting the funding source for project management activities derived from the State Budget appropriations;

+ A/C 46212- Financing for project execution: Reflecting the funding source for project execution activities derived from the State Budget appropriations.

- A/C 4622- Financing derived from grants and/or aids: Reflecting the funding source for projects derived from grants and/or aids.

This account is constituted by 2 following class-3 accounts:

+ A/C 46221- Financing for project management: Reflecting the funding source for project management activities derived from grants and/or aids;

+ A/C 46222- Financing for project execution: Reflecting the funding source for project execution activities derived from grants and/or aids.

- A/C 4628- Other financial sources: Reflecting funding sources for projects other than financing derived from the State Budget appropriations or grants and/or aids.

This account is constituted by 2 following class-3 accounts:

+ A/C 46281- Financing for project management: Reflecting other funding source for project management activities;

+ A/C 46282- Financing for project execution: Reflecting other funding source for project execution activities.

Article 8. Accounting for expenditure on projects

In A/C 662 – Expenditure on projects, class-2 accounts shall be reclassified as follows:

- A/C 6621- Expenditure derived from the State Budget appropriations: Reflecting expenditure on projects derived from the State Budget appropriations.

This account is constituted by 2 following class-3 accounts:

+ A/C 66211- Expenditure on project management: Reflecting expenses for project management activities derived from the State Budget appropriations;

+ A/C 66212- Expenditure on project execution: Reflecting expenses for project execution activities derived from the State Budget appropriations.

- A/C 6622- Expenditure derived from grants and/or aids: Reflecting expenses for projects derived from grants and/or aids.

This account is constituted by 2 following class-3 accounts:

+ A/C 66221- Expenditure on project management: Reflecting expenses for project management activities derived from grants and/pr aids;

+ A/C 66222- Expenditure on project execution: Reflecting expenses for project execution activities derived from grants and/or aids.

- A/C 6628- Expenditure derived from other financial sources: Reflecting expenses for projects derived from other funding sources other than either the State Budget appropriations or grants and/or aids.

This account is constituted by 2 following class-3 accounts:

+ A/C 66281- Expenditure on project management: Reflecting expenses for project management activities derived from other financial sources;

+ A/C 66282- Expenditure on project execution: Reflecting expenses for project execution activities derived from other financial sources.

Article 9. Unemployment insurance accounting

Account 332 – Payroll-related payables is supplemented with one following class-2 account:

A/C 3324- Unemployment insurance: Reflecting employer’s setting aside of a certain amount of money as contributions paid for unemployment insurance policies of public officials, servants and employees in accordance with unemployment insurance laws. A regulatory unit shall be obliged to maintain a detailed accounting book to keep track of and separately account for such unemployment insurance.

1. Structure and contents of the account 3324- Unemployment insurance

Debit side: The amount of unemployment insurance contribution which has been remitted to unemployment insurance fund authority;

Credit side:

- Setting aside a certain amount of money to pay for unemployment insurance contributions from expenses of a regulatory unit;

- Setting aside a certain amount of money withheld from salaries of public officials, servants and employees to pay for unemployment insurance contributions;

Credit balance: The amount of unemployment insurance contribution which has been set aside but has yet to be remitted to unemployment insurance fund authority.

2. Accounting method for certain key economic activities

- On a periodic basis, setting aside of a certain amount of money to pay for unemployment insurance contributions from expenses of a regulatory unit shall be entered into accounts as follows:

Debit A/C 661, 662, 631, 635, 241

Credit A/C 332 – Payroll-related payables (3324).

- Unemployment insurance contribution payables deducted from monthly salaries payable of public officials, servants and employees shall be recorded into accounts as follows:

Debit A/C 334- Payables to public servants and employees

Credit A/C 332 – Payroll-related payables (3324).

- Remitting the amount of unemployment insurance contributions to unemployment insurance fund authority shall be recorded into accounts as follows:

Debit A/C 332 – Payroll-related payables (3324)

Credit A/C 111, 112, 461, 462, 465.

If unemployment insurance contributions are derived from appropriations for expenditure on operations, programs and/or projects, this activity must be entered into accounts as follows: Credit A/C 008 "Appropriations for operating expenditure” or Credit A/C 009 “Appropriations for expenditure on programs and/or projects” (Off-balance sheet accounts).

Article 10. Accounting for overheads:

Supplementing the account 642 “Overheads”: Reflecting costs incurred from general administrative activities relating to public-sector service administration, production, business and other operations.

1. Bookkeeping disciplines:

- The account 642 shall only be kept by a regulatory unit whose overheads, once incurred from public service provision, production, business and other operations, can not be reasonably charged for specific users thereof due to which they are not immediately posted to expense-incurring entries;

- The account 642 must be kept in detail according to specific contents of expenses to meet managerial demands of the regulatory unit;

- At the end of an accounting period, accountants must calculate, carry forward and post overheads to relevant general expense accounts (such as A/C 631, A/C 635, A/C 661, etc.) in appropriate forms;

- A/C 642 shall not be kept in case overheads incurred are rationally charged for specific users thereof and directly posted to expense-incurring entries.

2. Structure and contents of the account 642- Overheads

Debit side: Overheads incurred within an accounting period.

Credit side:

- Entering decreases in overheads;

- Carrying forward and posting overheads to Debit side including related A/Cs such as A/C 631, 635, 661, 662, 241.

The account 642 does not have the closing balance.

3. Accounting method for certain key economic activities

- Overheads incurred which are not classified into specific users thereof shall be entered into accounts as follows:

Debit 642- Overheads

Credit relevant A/Cs.

- At the end of an accounting period, based on the table of distribution of overheads, accountants must calculate, carry forward and post overheads to relevant general expense accounts (such as A/C 631, A/C 635, A/C 661, etc.) in appropriate forms as follows:

Debit A/C 631 - Manufacturing and trading expenses

Debit A/C 635- Expenditure based on the Government commissioning

Debit A/C 661 – Operating expenditure

Debit A/C 662 – Project expenditure

Debit A/C 241- In-progress capital construction

Credit A/C 642- Overheads

Article 11. Accounting for difference between recurring income and expense

Deleting A/C 4211 "Difference between recurring income and expenses" and deleting section 2 of the accounting method for certain key economic activities referred to in A/C 421 “Outstanding difference between income and expense"

Changing the name and contents of the Account 004 “Authorized lump-sum administrative expense" as follows:

The account 004 “Difference between recurring income and expense”: Reflecting the differential amount between income gained and expense incurred from regular operations carried out by public administrative and public service units, and treatment of such difference.

1. Bookkeeping disciplines:

- Only entering into the Account 004 “Difference between recurring income and expense” the difference between income gained and expense incurred from regular operations due to the regulatory unit’s increase in income and limit on expenses with respect to the budget in which lump-sum administrative expenditure is authorized, or public administrative and public service units are accorded financial autonomy in accordance with financial regulations;

- Determination and utilization of difference between recurring income and expense must comply with applicable financial regulations.

The account 004 “Difference between recurring income and expense” accepts detailed entries in the previous and current year.

2. Structure and contents of the account 004- Difference between recurring income and expense

Debit side:

- Difference in which income is greater than expense with respect to regular operations due to increases in income and limit on expenses, temporarily determined by the regulatory unit within a given year (monthly or quarterly basis as referred to in financial regulations);

- Difference in which income is greater than expense with respect to regular operations according to the final accounts approved by competent authorities, greater than that temporarily determined by the regulatory unit within a given year;

- Difference in which income is greater than expense with respect to regular operations according to the final accounts approved by competent authorities, less than that temporarily determined within a given year (recording the negative number).

Credit side:

- Setting aside of a certain amount of money from funds or paying extra income according to financial regulations (the amount of money temporarily set aside within a given year and after the final accounts approved according to financial regulations).

Debit balance:

Reflecting difference where income gained from regular operations is greater than expenses incurred from these operations, which has not been used and is recorded as the closing balance.

3. Accounting method for certain key economic activities

- Within a given accounting year, based on the amount of income increases and expense limits with respect to the budget in which lump-sum administrative expenditure is authorized, or financial autonomy is accorded under financial regulations, accountants shall temporarily determine difference in which income gained from regular operations is greater than expenses incurred from these operations and enter it into accounts as follows:

Debit A/C 004 “Deference between recurring income and expense”

- Within a given accounting year, the regulatory unit’s temporary setting side of a certain amount of money from funds and payment of extra income by using difference where income gained from regular operations is greater than expenses incurred from these operations shall be entered into accounts as follows:

Debit A/C 661 – Operating expenditure

Credit A/C 431- Funds.

Credit A/C 334- Payables to public servants and employees

In addition, Credit A/C 004 “Deference between recurring income and expense”.

- In case the regulatory unit’s final accounts are approved by competent authorities:

+ If difference in which income is greater than expense with respect to regular operations according to the final accounts approved by competent authorities is greater than that temporarily determined by the regulatory unit within a given year, such difference shall be entered into accounts as follows:

Debit A/C 004 “Deference between recurring income and expense” (The increased portion as against the amount temporarily determined by the regulatory unit within a given accounting year).

The regulatory unit shall be entitled to set aside a certain amount of money from funds and pay extra income (The increased portion as against the amount temporarily set aside by that regulatory unit) and enter such extra income into accounts as follows:

Debit A/C 661 – Operating expenses (6611 – of the previous year)

Credit A/C 431- Funds.

Credit A/C 334- Payables to public servants and employees.

In addition, Credit A/C 004 “Deference between recurring income and expense”.

+ If difference in which income is greater than expense with respect to regular operations according to the final accounts approved by competent authorities is less than that temporarily determined by the regulatory unit within a given accounting year, such difference shall be entered into accounts as follows:

Debit A/C 004 “Deference between recurring income and expense” (recording the negative number) (The decreased portion as against the amount temporarily determined by the regulatory unit within a given accounting year).

Article 12. Amending and supplementing the accounting method for certain key economic activities:

1. Accounting for payment of salaries and other income paid through personal accounts

1.1. Accounting disciplines for payment of salaries and other income paid through personal accounts

- Payments given to public officials, servants and other employees via personal accounts, including salaries, wages, extra income and other payables like lunch expenses, allowances, bonuses, uniform costs and overtime pays, etc., must be sums from which social, unemployment and health insurance contributions, and advances that have not been used up, personal income tax that must be withheld and other amounts that must be withheld from salary payables (if any), must be subtracted.

In case there is any employee getting advances on their salaries, accountants must deduct the amount of advances from total salaries to calculate net salaries actually received; in case the amount of advances on salaries is greater than net salaries actually received, accountants must deduct such amount of advances from total salaries payable in the following month.

- When paying salaries and other earnings to public officials, servants and other employees in the regulatory unit through personal accounts, this unit must prepare accounting documents relating to salaries and other payables such as Salary payment statement (Form C02a- HD), Extra payment statement (Form C02b- HD), Bonus payment statement (Form C04- HD), Overtime pay statement (Form C07- HD). These accounting documents, once being used as the basis for calculation of salaries and other income payables to public officials, servants and other employees through their personal accounts, do not need the column “Signed by”. On a monthly basis, after consulting Salary payment and other earnings payment statements, accountants shall calculate salaries and other income payable to public officials, servants and other employees, and compile the list of salaries and earnings paid via personal accounts” (Form C13- HD) to request State Treasuries and banks to deposit money in these personal accounts.

- On a monthly basis, the regulatory unit must disseminate the said Salary payment statement, Extra payment statement, Bonus payment statement, Overtime pay statement to be widely known by all departments, divisions, groups, and public officials, servants and other employees in the regulatory unit (form of dissemination at the regulatory unit’s discretion).

1.2. Accounting method for certain key economic activities

- Remitting part of appropriations for operating and project expenditure in the State treasury to banking deposit accounts as payments for salaries and other income of public officials, servants and other employees via personal accounts shall be entered into accounts as follows:

Debit A/C 112 – Bank or State Treasury deposits (details of bank deposits)

Credit A/C 461, 462, 465.

In addition, Credit A/C 008 “Appropriations for operating expenditure” or A/C 009 “Appropriations for expenditure on programs and/or projects”

- Remitting part of money in deposit accounts opened at the State Treasury to deposit accounts opened at banks as payments for salaries and other income of public officials, servants and other employees via personal accounts shall be entered into accounts as follows:

Debit A/C 112 – Bank or State Treasury deposits (details of bank deposits)

Credit A/C Bank or State Treasury deposits (details of State Treasury deposits).

- Upon receipt of the service-providing Bank’s confirmation of the amount of salaries and other income deposited in personal accounts of specific public officials, servants and other employees, accountants shall enter such amount into accounts as follows:

Debit A/C 334- Payables to public servants and employees

Credit A/C 112 – Bank or State Treasury deposits (details of bank deposits).

2. Accounting for tangible fixed assets bought in bulk by higher-level units which are assigned to lower-level units

2.1. Accounting disciplines for in-bulk buying of tangible fixed assets

- Centralized purchase of tangible fixed assets by higher-level units must be carried out in accordance with applicable laws and regulations on procedures for arrangement for implementation, inspection, oversight and handling of violations relating to in-bulk buying of tangible fixed assets;

- Higher-level units must carry out procurement of fixed assets financed by the state budget in accordance with applicable regulations and assume responsibility for settlement and payment of expenses for centralized purchases of assets on the basis of appropriations given within an accounting year and actual completion of these purchases, allocations and transfers of tangible fixed assets to lower-level units, or otherwise higher-level units shall carry out this procurement and then authorize lower-level units to purchase, manage and use tangible fixed assets on the basis of appropriations given within an accounting year;

- Lower-level units must take into consideration procurement results of higher-level units when being authorized to purchase fixed assets; meanwhile, lower-level units must pay and settle expenses for purchase, management and utilization of tangible fixed assets in accordance with applicable laws and regulations.

2.2. Accounting method for certain key economic activities

2.2.1. Accounting for tangible fixed assets bought in bulk by higher-level units through bidding and procurement procedures and handed over to lower-level units for management and utilization

a. Accounting activities of higher-level units that organize procurement of tangible fixed assets in the form of centralized purchase or in-bulk buying

- Withdrawing part of appropriations for operating expenditure as advances paid to sellers as agreed upon in economic contracts for procurement of assets between the unit and supplier shall be entered into accounts as follows:

Debit A/C 331 – Payables (3311)

Credit A/C 112, 461…

In addition, Credit A/C 008 “Appropriations for operating expenditure”

- Upon completion of this procurement, based on the record of acceptance test of tangible fixed assets purchased which is signed by both the unit and supplier, invoices and relevant documents, accountants must enter value of purchased fixed assets as follows:

Debit A/C 241- In-progress capital construction (2411- Purchase of fixed assets)

Credit A/C 331 – Payables (3311)

- If costs relating to procurement of tangible fixed assets, such as consultancy, assistance, etc. costs, accountants must record them into accounts as follows:

Debit A/C 241- In-progress capital construction (2411- Purchase of fixed assets)

Credit A/C 111, 112

- Based on amounts which will be and have been paid, accountant shall determine the outstanding amounts that must be paid to suppliers of tangible fixed assets purchased and enter them into accounts as follows:

Debit A/C 331 – Payables (3311)

Credit A/C 112, 461…

In case of withdrawing part of appropriations for operating expenditure as payments to suppliers, accountants must also enter such part into Credit A/C 008 “Operating expenditure”.

- Upon handover of tangible fixed assets bought in the form of centralized purchase to lower-level units for their management and utilization, based on the decision on handover of assets, record of handover of assets and other relevant documents, accountants must keep track of such activities as follows:

Debit A/C 342- Internal payments (Details provided by specific lower-level units)

Credit A/C 241- In-progress capital construction (2411- Purchase of fixed assets)

- Upon receipt of lower-level unit’s report on full receipt of tangible fixed assets and relevant documents relating to tangible fixed assets handed over from higher-level units, accountants must record such activities into accounts as follows:

Debit A/C 661 – Operating expenditure

Credit A/C 342- Internal payments (Details provided by specific lower-level units)

- During the process of centralized purchase, higher-level units organize procurement in accordance with laws:

+ In case of revenues generated from sale of bidding documents and fees, accountants must record them into accounts as follows:

Debit A/C 111, 112

Credit A/C 511 – Receivables (5118)

+ In case of costs incurred from bidding and bid evaluation activities, accountant must record them into accounts as follows:

Debit A/C 511 – Receivables (5118)

Credit A/C 111, 112…

+ In case of carrying forward difference where income is greater than expense with respect to bidding and bid evaluation activities, accountants must record such difference into accounts as follows:

Debit A/C 511 – Receivables (5118)

Credit A/C 421 – Outstanding difference between income and expense (4218)

+ Upon receipt of the decision on treatment of difference where income is greater than expense, accountants must record such difference into accounts as follows:

Debit A/C 421 – Outstanding difference between income and expense (4218)

Credit relevant A/Cs.

b. Accounting activities of lower-level units that are authorized to manage and utilize tangible fixed assets purchased in the form of centralized purchase or in-bulk buying from higher-level units

- Upon receipt of tangible fixed assets assigned by higher-level units, based on the record of handover and receipt of assets attached to documents relating to tangible fixed assets, if these tangible fixed assets are immediately put into operation, accountants must record such activities into accounts as follows:

Debit A/C 211- Tangible fixed assets (The historical cost is the price at which these fixed assets are transferred and received from higher-level units)

Credit A/C 466- Funding source for formation of fixed assets.

- In case of tangible fixed assets that must be installed, tested and for which registration fees must be paid and other costs incurred from such installation and testing, accountants must record them into accounts as follows:

Debit A/C 241- In-progress capital construction (2411- Purchase of fixed assets)

Credit A/C 111, 112, 461.

In case of withdrawing part of appropriations for operating expenditure, accountants must also enter such part into Credit A/C 008 “Operating expenditure”.

- Upon completion of installation and testing, and handover of these assets for operation, accountants must reflect such activities into accounts as follows:

Debit A/C 211- Tangible fixed assets (The historical cost is the price at which these fixed assets are transferred and received from higher-level units, plus (+) installation and testing costs)

Credit A/C 241- In-progress capital construction (2411- Purchase of fixed assets) (including installation, testing, etc. costs)

Credit A/C 466- Funding source for formation of tangible fixed assets (at the price at which these fixed assets are transferred and received from higher-level units).

In addition,

Debit A/C 661 – Operating expenditure

Credit A/C 466- Funding source for formation of fixed assets (including installation, testing, etc. costs)

2.2.2. Accounting for tangible fixed assets bought in bulk through the process of higher-level units' organization of bidding for procurement and conclusion of contracts, and lower-level units’ purchase, management and utilization of these assets

a. Accounting activities of higher-level units that organize bidding for procurement of tangible fixed assets in the form of centralized purchase or in-bulk buying

- Higher-level units shall organize bidding and award the contract in accordance with laws:

+ In case of revenues generated from sale of bidding documents and fees, accountants must record them into accounts as follows:

Debit A/C 111, 112

Credit A/C 511 – Receivables (5118)

+ In case of costs incurred from bidding and bid evaluation activities, accountant must record them into accounts as follows:

Debit A/C 511 – Receivables (5118)

Credit A/C 111, 112…

+ In case of carrying forward difference where income is greater than expense with respect to bidding and bid evaluation activities, accountants must record such difference into accounts as follows:

Debit A/C 511 – Receivables (5118)

Credit A/C 421 – Outstanding difference between income and expense (4218)

+ Upon receipt of the decision on treatment of difference where income is greater than expense, accountants must record such difference into accounts as follows:

Debit A/C 421 – Outstanding difference between income and expense (4218)

Credit relevant A/Cs.

a. Accounting activities of lower-level units that purchase, manage and utilize tangible fixed assets)

- Based on documents relating to purchase of fixed assets that are immediately brought into operation, including fixed asset purchase invoices and other payment documents, accountants shall determine the historical cost of these assets and prepare the record of handover and receipt of fixed assets as well as enter them into accounts as follows:

Debit A/C 211- Tangible fixed assets

Credit A/C 111, 112, 461.

In case of withdrawing part of appropriations for operating expenditure, accountants must also enter such part into Credit A/C 008 “Operating expenditure”.

In addition,

Debit A/C 661 – Operating expenditure

Credit A/C 466- Funding source for formation of fixed assets

- When fixed assets purchased must be installed or tested, accountants must record such activities into accounts as follows:

Debit A/C 241- In-progress capital construction (2411- Purchase of fixed assets)

Credit A/C 111, 112, 461.

In case of withdrawing part of appropriations for operating expenditure, accountants must also enter such part into Credit A/C 008 “Operating expenditure”.

Upon completion of installation and handover of these assets to be put into operation, accountants must reflect such activities into accounts as follows:

Debit A/C 211- Tangible fixed assets

Credit A/C 241- In-progress capital construction (2411- Purchase of fixed assets)

In addition,

Debit A/C 661 – Operating expenditure

Credit A/C 466- Funding source for formation of fixed assets

3. Accounting for products or goods for internal consumption

With respect to products or goods for internal consumption which are those produced or supplied for consumption by the regulatory unit itself, except for those used for further production and business processes, determination of VAT tax amounts which are deducted and must be paid, and declaration of VAT tax and corporate income tax shall be carried out in accordance with laws on taxes.

- If products or goods which are taxed with VAT tax calculated according to the credit-invoice method are used for internal consumption or further production and trading of goods and services subject to VAT tax calculated according to the credit-invoice method, upon dispatching of these goods and products for internal consumption, accountants must record them into accounts as follows:

Debit A/C 631 – Expenditure on production and business operations (expenses for manufacturing of products or cost price of goods)

Credit A/C 531 – Revenues generated from production and business operations (reflecting revenue gained from internal sale of goods at the cost of manufacturing of products or cost price of goods).

In addition, the cost price of goods sold is carried forward into accounts as follows:

Debit A/C 531 – Revenue generated from production and business activities

Credit A/C 155 – Products or goods.

In addition, accountants must declare VAT tax on products and goods for internal consumption which is deducted and enter such tax into accounts as follows:

Debit A/C 311 – Receivables (3113)

Credit A/C 333 – Payables to the Government (33311).

- If products or goods which are taxed with VAT tax calculated according to the credit-invoice method are used for internal consumption or further production and trading of goods and services not subjected to VAT tax calculated or subjected to VAT tax calculated according to the subtraction method, upon dispatching of these goods and products for internal consumption, accountants must record them into accounts as follows:

Debit A/C 631 – Expenditure on production and business operations (expenses for manufacturing of products or cost price of goods, plus (+) output VAT tax)

Credit A/C 531 – Income gained from manufacturing and business operations (reflecting revenue generated from internal sale of goods at the cost of manufacturing of products or the cost price of goods).

Credit A/C 3331- VAT tax payable.

In addition, the cost price of goods sold is carried forward into accounts as follows:

Debit A/C 531 – Income gained from manufacturing and business operations

Credit A/C 155 – Products or goods.

Article 13. Amending the third part – Accounting records

1. In Logbook of budget estimates (Form S41-H), Logbook of usage of expenditure (Form S42- H), General book of expenditures (Form S43- H), Detailed logbook of operating expenditure (Form S61- H), Detailed logbook of project expenditure (Form S62- H), General logbook of final accounts of budget and other funding sources of a regulatory unit (Form S04- CT-H), the fields (columns) Type or Item shall be replaced by “Code of economic sector”; the fields (columns) Group, Subgroup, Division or Subdivision shall be replaced by “Code of economic activity” (in particular, in the part I- Logbook of budget estimates, the field “Group" may not be left blank).

2. Supplementing “Logbook of overheads (Form S73- H) (in the Appendix 02.1).

Article 14. Amending the forth section- System of financial statements.

1. In the top left corner of templates of financial statements, Code of the unit using the state budget is replaced by "Code of the unit affiliated with the state budget”;

2. In the "General report on expenditure and final accounts of used expenses” (Form B02- H) (Form B02/CT-H) and auxiliary templates of “Detailed report on operating expenditure” (Form F02-1H); “Detailed report on project expenditure” (Form F02-2H); “Comparison chart of budget estimates at the state treasury” (Form F02-3aH) and “Comparison chart of advances and payment of advances on the budget expenditure at the state treasury” (Form F02-3bH); “General report on final accounts of budget expenditure and other sources in a regulatory unit" (Form B04/CT-H), the fields (columns) Type, Item shall be replaced by “Code of economic sector”, and the field (column) Group, Subgroup, Division, Subdivision shall be replaced by “Code of economic activity”.

- Amending the auxiliary chart F02- 3aH “Comparison chart of budget estimates at the state treasury” (in the Appendix 03.1);

- Supplementing the auxiliary chart F02- 3cH “Comparison chart of balances of deposit accounts” (in the Appendix 03.2).

3. Amending and supplementing “Notes on financial statements” (Form B06- H) as follows:

- In Part V “Status of usage of budget estimates”, Part VI “State budget fees and charges collected by a regulatory unit and retained for coverage of expenses", Part VII "Status of receipt of budget expenditure", the fields (columns) Type, Item shall be replaced by the field (column) “Code of economic sector”;

- In Part IV “Status of remittance of budget receipts to the state budget and higher-level units”: Adding column 1 (after column B- Indicator) "Previous year’s amounts payable carried forward”; replacing Column 1 “Amounts payable" by Column 2 “This year’s amounts payable”; replacing Column 2 “Amounts which have been paid in” by Column 3 “Amounts which have been paid in this year”; replacing Column 3 “Remaining amounts that must be paid in” by Column 4 “Remaining amounts that must be paid in this year” (in the auxiliary chart 03.3).

Article 15. This Circular shall take effect after 45 days from the signature date. Other accounting parts related to but not subject to guidance in this Circular shall be carried out by public administrative and public service units in the same manner as in the public-sector administrative accounting regulations issued together with the Decision No. 19/2006/QD-BTC of the Minister of Finance dated March 30, 2006.

Article 16. Public administrative and public service units adopting the particular accounting system under particular Circular issued by the Ministry of Finance, particular Decision or Approval Instrument, must refer to this Circular to provide proper guidelines and perform suitable amendments.

Article 17. Ministries, sectoral authorities, People’s Committees, Departments of Finance, State Treasuries of centrally-affiliated cities and provinces shall be responsible for providing guidance to regulatory units to implement this Circular. In the course of implementation of this Circular, if there is any difficulty that may arise, timely feedbacks must be punctually submitted to the Ministry of Finance for further consideration and possible solutions./.

| PP. THE MINISTER |

------------------------------------------------------------------------------------------------------

This translation is made by LawSoft and for reference purposes only. Its copyright is owned by LawSoft and protected under Clause 2, Article 14 of the Law on Intellectual Property.Your comments are always welcomed