Circular No. 67/2012/TT-BTC adjusting the preferential import tax rate on stainl đã được thay thế bởi Circular No.193/2012/TT-BTC promulgating the preferential import and export tari và được áp dụng kể từ ngày 01/01/2013.

Nội dung toàn văn Circular No. 67/2012/TT-BTC adjusting the preferential import tax rate on stainl

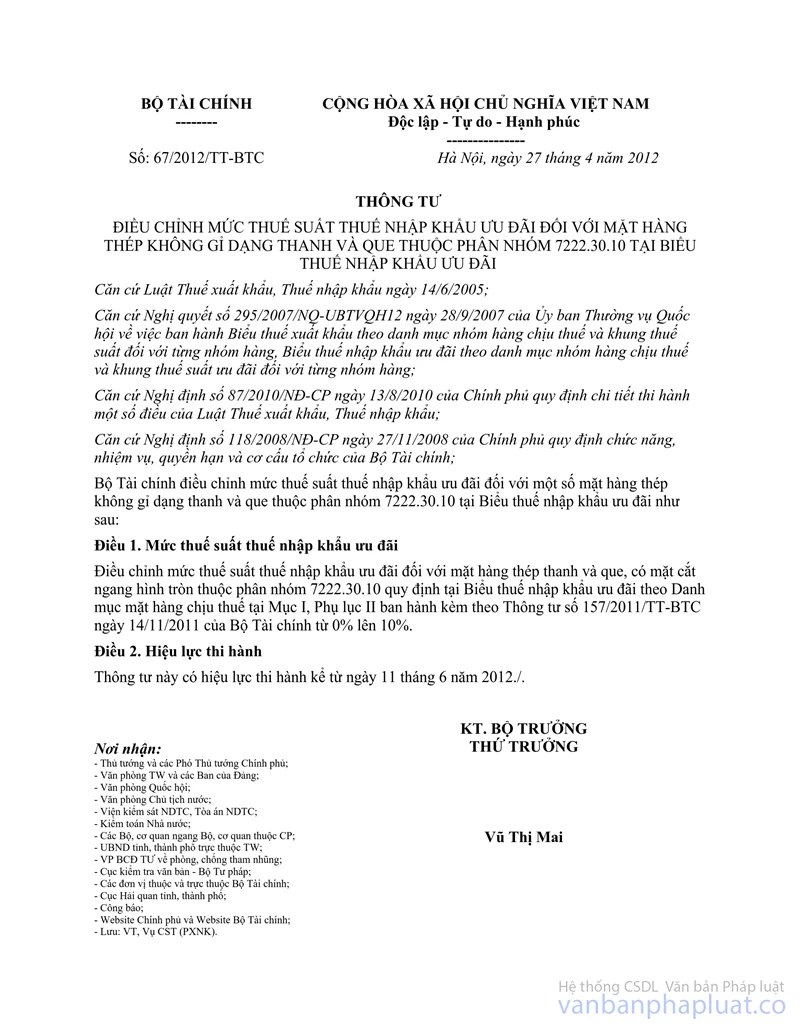

THE MINISTRY OF FINANCE | THE SOCIALIST REPUBLIC OF VIETNAM |

No. 67/2012/TT-BTC | Hanoi, April 27, 2012 |

CIRCULAR

ADJUSTING THE PREFERENTIAL IMPORT TAX RATE ON STAINLESS STEEL BARS AND RODS BELONGING TO THE SUBGROUP 7222.30.10 OF THE PREFERENTIAL IMPORT TARIFF

Pursuant to the Law on Import Duty and Export Duty on June 14, 2005;

Pursuant to the National Assembly Standing Committee's Resolution No. 295/2007/NQ-UBTVQH12 on September 28, 2007, promulgating the Export Tariff by the list of taxable commodity groups and the tax bracket on each commodity group, the Preferential Import Tariff by the list of taxable commodity groups and the preferential duty bracket on each commodity group;

Pursuant to the Government's Decree No. 87/20I0/ND-CP on August 13, 2010, detailing a number of articles of the Law on Import Duty and Export Duty;

Pursuant to the Government's Decree No. 118/2008/ND-CP on November 27, 2008, defining the functions, tasks, powers and organizational structure of the Ministry of Finance;

The Ministry of Finance adjusts the preferential import tax rate on some kinds of stainless steel bars and rods belonging to the subgroup 7222.30.10 of the Preferential Import Tariff as follows:

Article 1. Preferential import tax rates

The preferential import tax rate on cylindrical stainless steel bars and rods belonging to the subgroup 7222.30.10 of the Preferential Import Tariff in the list of taxable commodity groups in Section I, Appendix II promulgated together with the Ministry of Finance's Circular No. 157/2011/TT-BTC on November 14, 2011 is adjusted from 0% to 10% .

Article 2. Effect

This Circular takes effect on June 11, 2012./.

| FOR THE MINISTER |

------------------------------------------------------------------------------------------------------

This translation is made by LawSoft, for reference only. LawSoft is protected by copyright under clause 2, article 14 of the Law on Intellectual Property. LawSoft always welcome your comments