Law No. 17-L/CTN, amending and supplementing a number of articles of the Law on Import tax and Export tax, passed by The National Assembly. đã được thay thế bởi Law No. 45/2005/QH1 of June 14, 2005, on import tax and export. và được áp dụng kể từ ngày 01/01/2006.

Nội dung toàn văn Law No. 17-L/CTN, amending and supplementing a number of articles of the Law on Import tax and Export tax, passed by The National Assembly.

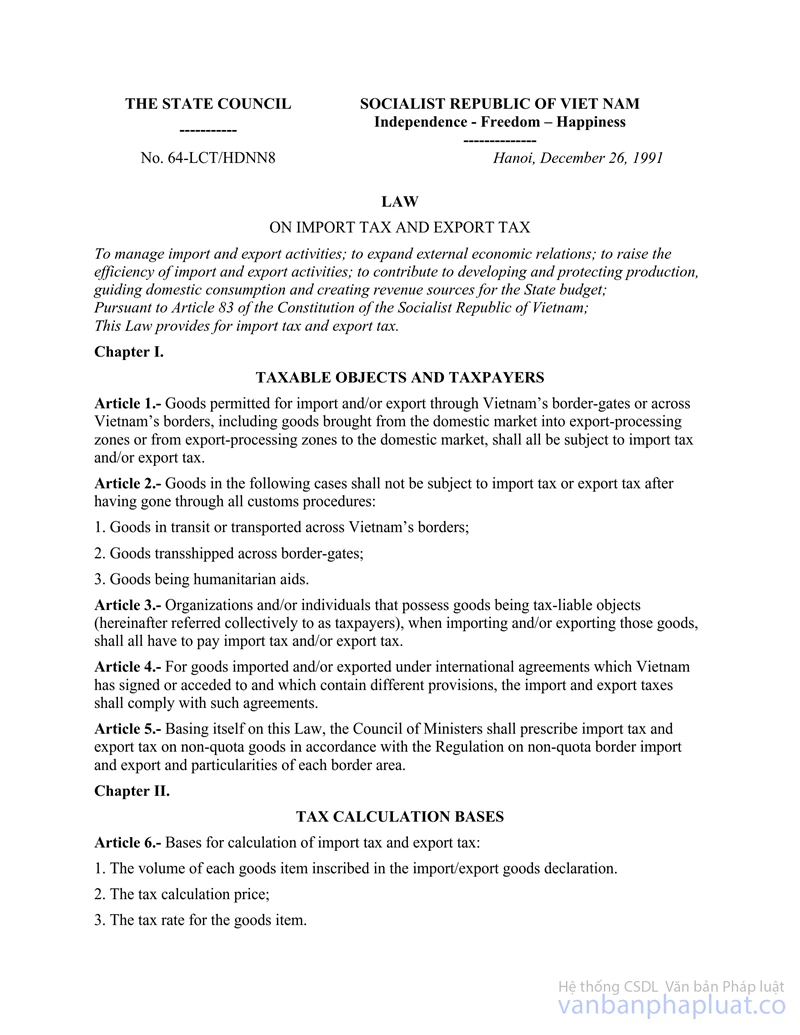

THE STANDING COMMITTEE OF NATIONAL ASSEMBLY | SOCIALIST REPUBLIC OF VIET NAM |

No. 17-L/CTN | Hanoi, July 5, 1993 |

LAW

AMENDING AND SUPPLEMENTING A NUMBER OF ARTICLES OF THE LAW ON IMPORT TAX AND EXPORT TAX

Pursuant to Article 84 of the 1992 Constitution of the Socialist Republic of Vietnam;

This Law amends and supplements a number of articles of the Import Tax and Export Tax Law passed on December 26, 1991 by the National Assembly of the Socialist Republic of Vietnam.

Article 1.- To amend and supplement a number of articles of the Law on Import Tax and Export Tax as follows:

1. Article 2 is amended as follows:

“Article 2.- Goods in the following cases shall not be subject to import tax or export tax after having gone through all customs procedures:

1. Goods in transit or transshipped across Vietnam’s borders; goods transported across border-gates under the Government’s regulations;

2. Article 10 is amended as follows:

“Article 10

1. Non-refundable aid goods;

2. Goods temporarily imported for re-export or temporarily exported for re-import for participation in trade fairs or exhibitions;

3. Goods being assets on the move.

4. Import/export goods of foreign organizations and/or individuals that are entitled to immunities prescribed by the Council of Ministers in accordance with international agreements which Vietnam has signed or acceded to;

5. Goods being supplies or raw materials imported for processing for,

3. Article 11 is amended as follows

“Article 11

1. Goods imported for exclusive use in direct service of security, national defense, scientific research, and education and training.

2. Goods imported or exported by foreign-invested enterprises and foreign parties to business cooperation contracts, in special cases where investment should be encouraged.

The State Commission for Cooperation and Investment shall, after reaching agreement with the Finance Ministry, consider the exemption of import tax or export tax for each special case where investment should be encouraged.

4. To add to the end of Clause 5, Article 14, the following:

“Goods temporarily imported for re-export shall not be liable to export tax upon re-export; goods temporarily exported for re-import shall not be liable to import tax upon re-import.”

5. Points a and b, Clause 3 of Article 17

“3.

For goods temporarily exported for re-import under permission of the competent State agency, if they are actually re-imported within the 15-day time limit prescribed at this Point, they shall not be liable to export tax.

For goods temporarily imported for re-export under permission of the competent State agency, if they are actually re-exported within the 30-day time limit prescribed at this Point, they shall not be liable to import tax.

Particularly for supplies and raw materials imported for the production of exports, the time limit for full payment of taxes shall be specified for each production branch, which, however, shall not exceed 90 days as from the date a taxpayer receives the tax-collecting agency’s official notice of the payable tax amount. The Government shall specify time limit applicable to each production branch.

In cases where goods made from the imported supplies or raw materials have actually been exported within the time limit prescribed at this Point, the import tax shall not be paid;”

6. Clause 1 of Article 20 is amended as follows:

“1. Each day after the tax-payment time limit prescribed in Article 17 of this Law, if taxpayers fail to pay taxes, they shall have to pay fines equal to 0.2% of the tax arrears.”

7. The words “State Council” and “Ministers’ Council” are amended into “National Assembly Standing Committee” and “Government” respectively.

Article 2.- The Government shall amend and/or supplement documents detailing the implementation of the promulgated Law on Import Tax and Export Tax to make it suitable to this Law.

Article 3.- This Law takes effect as from September 1, 1993.

This Law was passed on July 5, 1993 by the IXth National Assembly of the Socialist Republic of Vietnam

NATIONAL ASSEMBLY |