Nội dung toàn văn Official Dispatch No. 2721/TCT-CS of July 17, 2008, on Value-added tax on securities companies’ operations

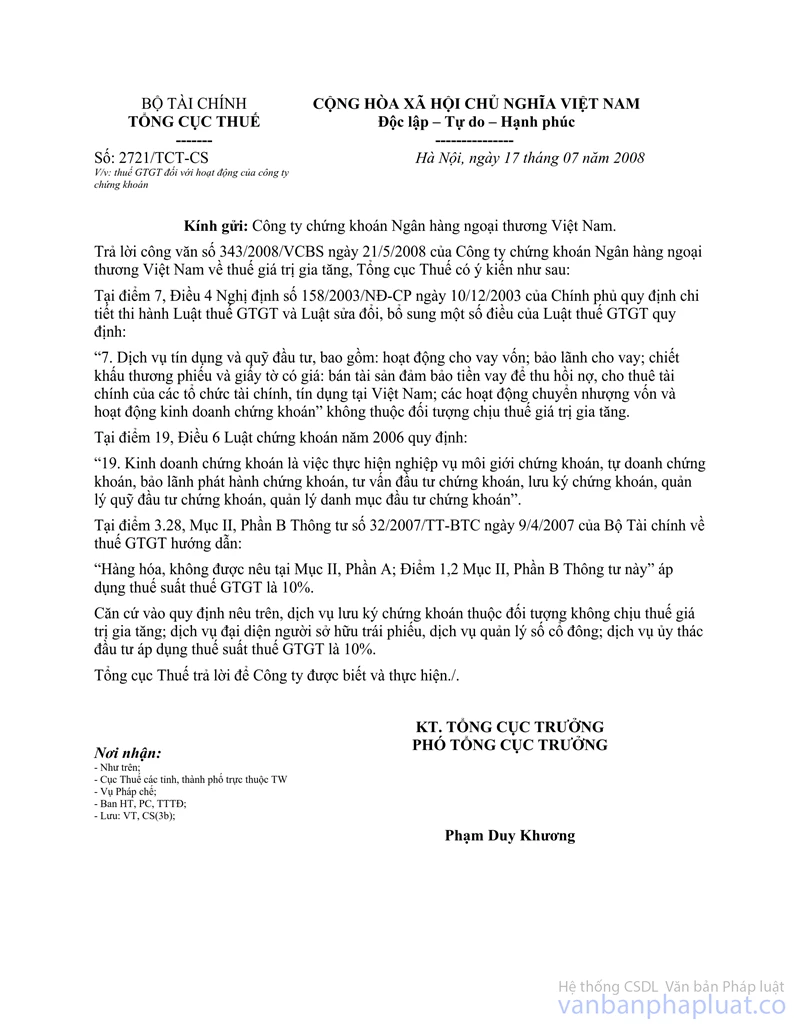

MINISTRY OF FINANCE | SOCIALIST REPUBLIC OF VIET NAM |

No. 2721/TCT-CS | Hanoi, July 17, 2008 |

To: The Bank for Foreign Trade of Vietnam (Vietcombank) Securities Company

In response to Vietcombank Securities Company’s Official Letter No. 343/2008/VCBS of May 21, 2008, on value-added tax, the General Department of Taxation gives the following opinions:

Point 7, Article 4 of the Government’s Decree No. 158/2003/ND-CP of December 10, 2003, detailing the implementation of the Value-Added Tax Law and the Law Amending and Supplementing a Number of Articles of Value-Added Tax Law, stipulates:

“7. Credit services and investment funds, including capital lending activities; loan guarantee; discount of negotiable instruments and valuable papers; sale of loan security assets for debt retrieval, financial leasing by Vietnam-based financial and credit institutions; capital transfer and securities trading activities” are not subject to value-added tax.

Point 19, Article 6 of the 2006 Securities Law, stipulates:

“19. Securities business means the performance of such professional operations as securities brokerage, securities dealing, securities issuance underwriting, securities investment consultancy, securities depository, securities investment fund management or portfolio management.”

Point 3.28, Section II, Part B of the Finance Ministry’s Circular No. 32/2007/TT-BTC of April 9, 2007, on value-added tax, guides:

“Goods not specified in Section II, Part A; and Points 1 and 2, Section II, Part B of this Circular” are subject to the value-added tax rate of 10%.

Under the above provisions, securities depository services are not subject to VAT; services of representative of bond owners, services of management of shareholder books; and services of entrusted investment shall be subject to the VAT rate of 10%.

The General Department of Taxation gives above answer to the Company for information and implementation.

| FOR THE GENERAL DIRECTOR OF TAXATION |