Nội dung toàn văn Circular No. 83/2012/TT-BTC on guiding exemption, reduction and prolongation

|

THE

MINISTRY OF FINANCE |

THE

SOCIALIST REPUBLIC OF VIETNAM |

|

No. 13/NQ-CP">83/2012/TT-BTC |

Hanoi, May 23, 2012 |

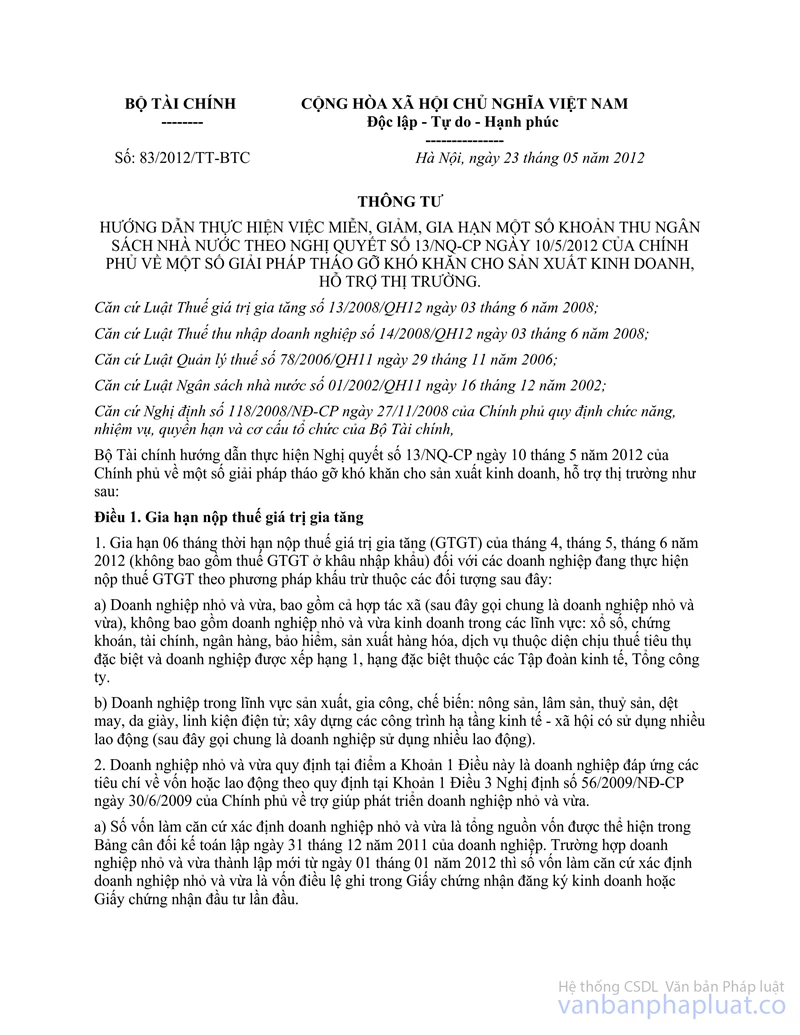

CIRCULAR

ON GUIDING EXEMPTION, REDUCTION AND PROLONGATION OF TIME LIMIT FOR A NUMBER OF STATE BUDGET REVENUES ACCORDING TO THE GOVERNMENT’S RESOLUTION NO. 13/NQ-CP OF MAY 10, 2012, ON A NUMBER OF SOLUTIONS TO REMOVE DIFFICULTIES IN PRODUCTION, BUSINESS AND MARKET SUPPORT.

Pursuant to the Law on Value-added tax No.13/2008/QH12 of June 03, 2008;

Pursuant to the Law on Enterprise income tax No.14/2008/QH12 of June 03, 2008;

Pursuant to the Law on Tax administration No. 78/2006/QH11 of November 29, 2006;

Pursuant to the Law on State budget No. 01/2002/QH11 of December 16, 2002;

Pursuant to the Government's Decree No. 118/2008/ND-CP on defining the functions, tasks, powers and organizational structure of the Ministry of Finance,

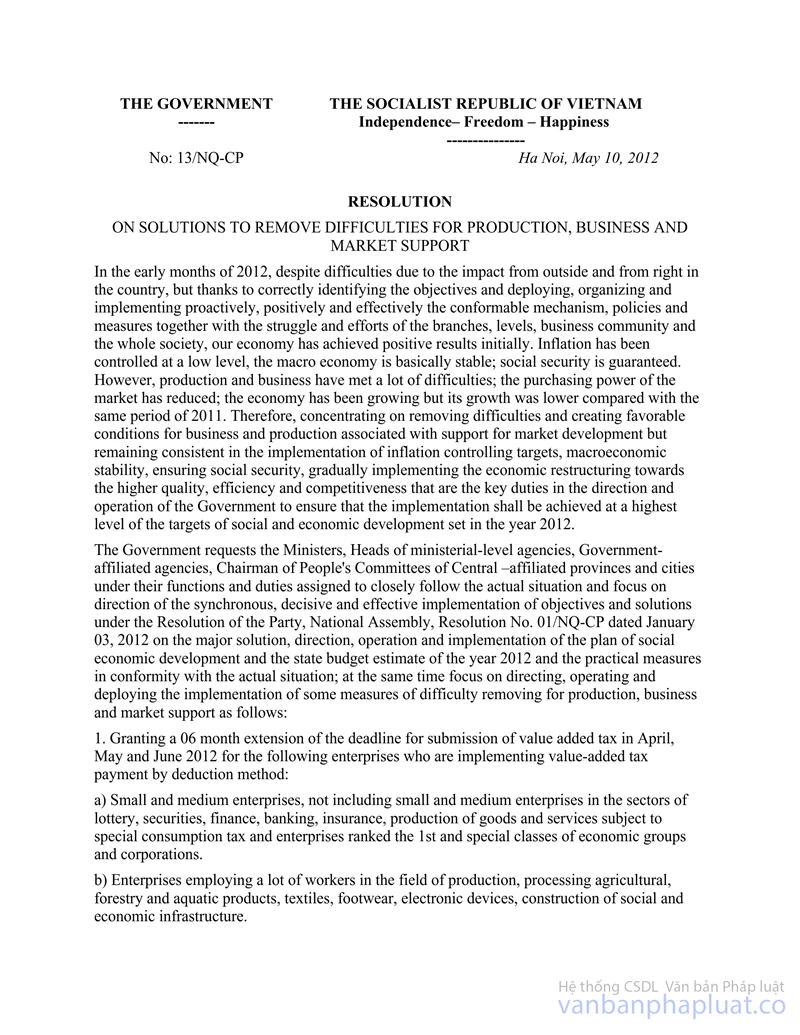

The Ministry of Finance guides the implementation of the Government’s resolution no.13/NQ-CP of May 10, 2012 on a number of solutions to remove difficulties for production, business and market support as follows:

Article 1. Prolongation of the value-added tax payment time limit

1. Prolonging the deadlines of the value-added tax (VAT) payment of April, May and June of 2012 for 06 months (excluding VAT of the importation stage) regarding enterprises paying VAT under the deduction method being the following subjects:

a) The small- and medium-sized enterprises including cooperatives (hereinafter referred to as small- and medium-sized enterprises), excluding small- and medium-sized enterprises that business in fields of: lottery, securities, finance, banking, insurance, or producing excise tax-liable goods, services and first-class, special-class enterprises belonging to Corporations or General companies.

b) Enterprises producing, processing agricultural-forestry-fishery products, textile and garment, leather and footwear, electronic components, building socio-economic infrastructure that use plenty of workers (hereinafter referred to as labor-intensive enterprises)

2. Small- and medium-sized enterprises prescribed in point a Clause 1 this Article are enterprises that satisfy the criteria of capital or labour prescribed in Clause 1 Article 3 of the Government's Decree No. 56/2009/ND-CP of June 30, 2009 on supporting the development of small- and medium-sized enterprises.

a) The capital being the basis for categorizing as small- and medium-sized enterprises is the total capital identified in the accounting balance sheet made on December 31, 2011 of the enterprises. For small- and medium-sized enterprises established from January 01, 2012, the capital being the basis for categorizing as small- and medium-sized enterprises is the charter capital written in the First Business registration certificate or the investment certificate.

b) The annual average number of laborers being the basis for categorizing as small- and medium-sized enterprises (including laborers of branches and affiliated units) is the number of laborers used regularly by enterprise in 2011, excluding laborers under contracts of short-term of less than 3 months.

The annual average number of laborers used regularly is determined as guides in the Circular No. 40/2009/TT-BLDTBXH of December 03, 2009 of the Ministry of Labour, War Invalids and Social Affairs on guiding the calculation of number of laborers used regularly under the Government's Decree No. 108/2006/ND-CP of September 22, 2006 on detailing and guiding the implementation of a number of articles of the Law on Investment.

For enterprises established from January 01, 2012, the total of laborers, excluding laborers under contracts of short-term of less than 3 months, is calculated from the date of establishment until April 30, 2012 (if established before May 2012), or till May 31, 2012 (if established before June 2012), or till June 30, 2012 (if established before July 2012).

c) For enterprises operating various business lines, the categorization of small- and medium-sized enterprises to determine the criterion of capital or labour as prescribed in the Decree No. 56/2009/ND-CP shall be based on the primary business line written in their Business registration certificate. If the primary business line is not able to be identified, one of the following criterions shall be used to identify the primary business line of the enterprise:

- The most number of laborers working in each business line of the enterprise in 2011.

- The highest turnover from each business line of the enterprise in 2011.

In case using the above criterions but the primary business line being the basis for categorizing as small- and medium-sized enterprises is still unable to be identified, it is required to base on the criterion of smallest capital or number of laborers of the business line among the business lines operated by the enterprise in 2011 as prescribed in Clause 1 Article 3 of the Decree No. 56/2009/ND-CP.

d) The 06-month prolongation of the deadline of VAT payment is not applicable to the following subjects:

d.1) Small- and medium-sized enterprises operate business of lottery, securities, finance, banking, insurance, or producing excise tax-liable goods, services.

In case the small- and medium-sized enterprise operating the business of lottery, securities, finance, banking, insurance, or producing excise tax-liable goods, services operates business or production subject to VAT of which the payment is prolonged apart from the business of lottery, securities, finance, banking, insurance, or producing excise tax-liable goods, services, the VAT amount payable of the other business or production shall be prolonged and calculated as follows:

|

Prolonged VAT amount in month |

= |

VAT amount payable under the declaration of prolonged month |

x |

Turnover subject to VAT from prolonged activity in month |

|

Total turnover from goods, services subject to VAT in month |

d.2) First-class enterprises as prescribed in the Joint Circular No. 23/2005/TTLT-BLDTBXH-BTC of August 31, 2005 of the Ministry of Labour, War Invalids and Social Affairs and the Ministry of Finance on guiding the ranking and salaries of Directorate members, General Directors, Directors, Deputy General Directors, Deputy Directors and Chief accountants of State companies.

d.3.) Special-class enterprises prescribed in the Prime Minister’s Decision No. 185/TTg of March 28, 1996 on special-class State companies and the Prime Minister’s Decision No. 186/TTg of March 28, 1996 on the list of special-class State companies.

d.4) Economic organizations being non-business units

3. Labor-intensive enterprises (including laborers of branches and affiliated units) operating in the business lines which the VAT payment is prolonged prescribed in point b Clause 1 this Article, include:

a) Enterprises employed in 2011 more than 300 regular laborers, excluding laborers under contracts of short-term of less than 3 months regarding enterprises established before January 01, 2012.

For enterprises established from January 01, 2012, the total of laborers is over 300 people, excluding laborers under contracts of short-term of less than 3 months, calculated from the date of establishment until April 30, 2012 (if established before May 2012), or May 31, 2012 (if established before June 2012), or June 30, 2012 (if established before July 2012).

The production and processing of agricultural-forest-fishery products, textile and garment, leather and footwear, electronic components prescribed in point b Clause 1 this Article is determined basing on the provisions in the Vietnam economic sector system promulgated together with the Prime Minister’s Decision No. 10/2007/QD-TTg of January 23, 2007.

Activities of construction of socio-economic infrastructure prescribed in point b Clause 1 this Article include construction and installation of water plants, power plants, electricity transmission and distribution works, water supply and drainage systems; roads, railroads; airports, seaports, river ports; air terminal, train stations, bus stations; schools, hospitals, cultural houses, cinemas, art performance centers, sport training and competition facilities; wastewater and solid waste treatment system; information and communication works, irrigation works serving agriculture, forestry and aquiculture.

b) For Labor-intensive enterprises operating production and business in sectors which the tax payment is not prolonged, the prolonged VAT amount is calculated as follows:

|

Prolonged VAT amount in month |

= |

VAT amount payable under the declaration of prolonged month |

x |

Turnover subject to VAT of prolonged business sector in month |

|

Total turnover of goods, services subject to VAT in month |

4. Branches, affiliated units of small- and medium-sized enterprises and labor-intensive enterprises which are not in the same province of the head office (excluding units having activities of construction, installation, sale as extra-provincial business declare VAT for temporary calculation under rates 1%, 2%) separately making VAT declaration with the tax agencies directly managing the branches and affiliated units are also subjects of prolongation of VAT payment.

The branches and affiliated units not having activities of production and business in sectors which the tax payment is prolonged are not subjects of prolongation of VAT payment.

Enterprises shall make lists of branches and affiliated units (specifying the name, address, tax code, number of laborers and business line of each branch) and inform the list to the tax agencies directly managing such branches and affiliated units. Enterprises are responsible before law for the accuracy of the List of branches and affiliated units being sent to tax agencies.

5. Enterprises being subjects of prolongation of VAT payment as guided in this Article shall make and send the VAT declaration in April, May and June 2012 but do not have to pay the VAT amount payable written on the declared VAT declaration.

- The time limit to pay VAT of April 2012 is November 20, 2012 at the latest.

- The time limit to pay VAT of May 2012 is December 20, 2012 at the latest.

- The time limit to pay VAT of June 2012 is January 21, 2013 at the latest.

6. Enterprises must identify by themselves whether they being the subjects of prolongation of VAT payment, the prolonged VAT amount and make declaration in Annex 1 (promulgated together with this Circular) and send it with the VAT declaration of the prolonged month.

Enterprises having submitted the VAT declaration of April 2012 but having not made Annex 1 stated above must make and sent in addition to tax agencies. Within the term prolonged of tax payment, units shall not be fined because of delaying the tax payment.

Article 2. Reducing land rent

1. Reducing 50% of the land rent payable in 2012 regarding economic organizations, enterprises operating in commerce and service business renting land from the State paying annual land rent under land rent rates prescribed in the Government's Decree No. 121/2010/ND-CP of December 03, 2010. The reduction is implemented as prescribed in the Prime Minister’s Decision No. 2093/QD-TTg of November 23, 2011.

2. The conditions, order, procedures and authority to reduce land rent are implemented as prescribed in the Official Dispatch No. 17969/BTC-QLCS of December 30, 2011 of the Ministry of Finance and the Ministry of Finance’s documents on guiding the Prime Minister’s Decision No. 2093/QD-TTg of November 23, 2011.

Article 3. Prolongation of enterprise income tax payment

1. Prolonging the enterprise income tax payment terms for 09 months regarding the enterprise income tax amount payable in 2010 or earlier that until May 10, 2012, the following enterprises still fail to pay State budget remittances:

a) Small- and medium-sized enterprises (including cooperatives), excluding small- and medium-sized enterprises that operate the business of lottery, securities, finance, banking, insurance, or producing excise tax-liable goods, services and first-class, special-class enterprises belonging to Corporations or General companies.

b) Enterprises producing, processing agricultural-forestry-fishery products, textile and garment, leather and footwear, electronic components, building socio-economic infrastructure that are labor-intensive enterprises

c) Enterprises producing mechanical products being means of production, means of waterway transportation, (including inland waterway and sea transportation), steel, cement; small- and medium-sized enterprises operating real estate business.

Payment delaying shall not be fined within the period from January 01, 2012 until the end of September 30, 2012 regarding the enterprise income tax amounts having not been paid of enterprises prescribed in this Clause. If the tax agency has notified the fine for payment delaying, the tax agency shall notify again the fine for payment delaying.

On October 01, 2012, enterprises must pay the enterprise income tax amount that has been prolonged prescribed in this Clause.

Before October 01, 2012, if competent agencies check, inspect and detect that the enterprise income tax amount of the prolonged term prescribed in this Clause is more than the declared amount, or that amount is not declared, enterprise shall be prolonged for the detected additional enterprise income tax amount until the end of September 30, 2012, and the payment delaying shall not be fined within the period from January 01, 2012 until the end of September 30, 2012.

From October 01, 2012, if competent agencies check, inspect and detect that the enterprise income tax amount of the deferment term prescribed in this Clause is more than the declared amount, or that amount is not declared, the payment delaying of the detected additional enterprise income tax amount shall not be fined within the period from January 01, 2012 until the end of September 30, 2012.

2. Prolonging the enterprise income tax payment terms for 09 months regarding the enterprise income tax amount payable in 2011 that has not been remitted to the State budget of enterprises producing mechanical products being means of production, means of waterway transportation, (including inland waterway and sea transportation), steel, cement (except for small- and medium-sized enterprises operating in this business sector); small- and medium-sized enterprises operating real estate business

Payment delaying is not fined within the period from April 01, 2012 until the end of December 31, 2012 regarding the enterprise income tax amount not being remitted to the State budget of the enterprises prescribed in this Clause. If the tax agency has notified the fine for payment delaying, the tax agency shall notify again the fine for payment delaying.

On January 02, 2013, enterprises must pay enterprise income tax regarding the prolonged amount prescribed in this Clause.

Before January 01, 2013, if competent agencies check, inspect and detect that the enterprise income tax amount of the prolonged term prescribed in this Clause is more than the declared amount, or that amount is not declared, the detected additional enterprise income tax amount shall be prolonged until the end of December 31, 2012, and the payment delaying shall not be fined within the period from April 01, 2012 until December 31, 2012.

From January 01, 2013, if competent agencies check, inspect and detect that the enterprise income tax amount of the deferment term prescribed in this Clause is more than the declared amount, or that amount is not declared, the payment delaying of the detected additional enterprise income tax amount shall not be fined within the period from April 01, 2012 until December 31, 2012.

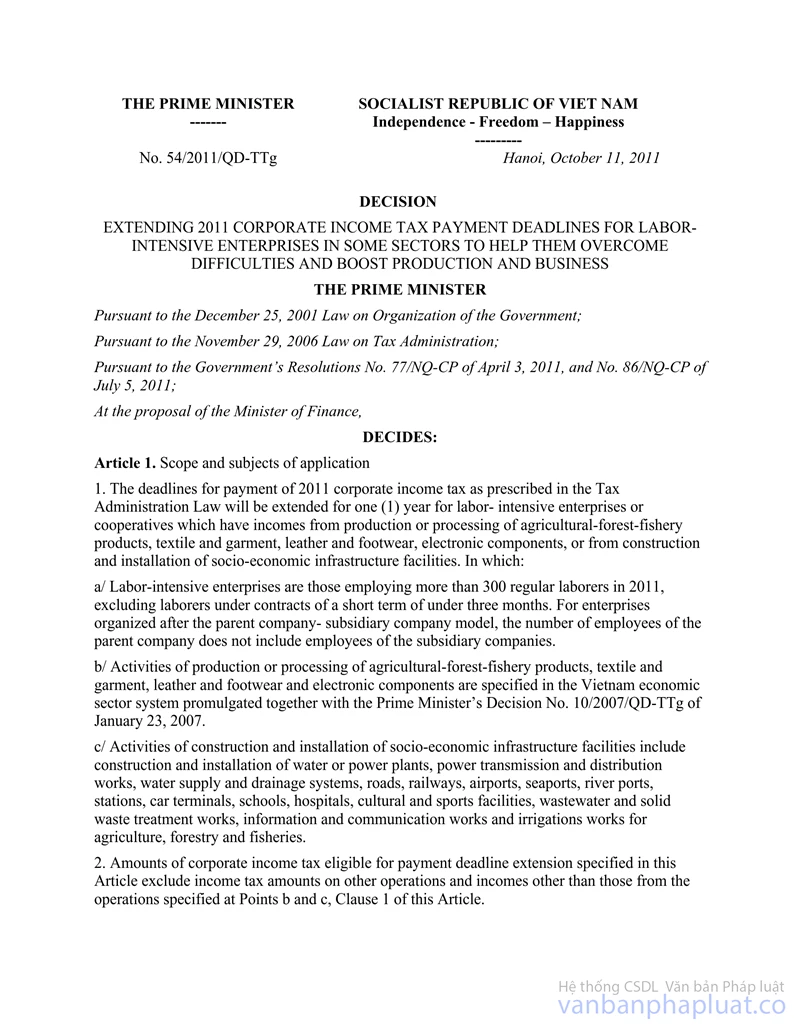

3. The enterprise income tax amount payable in 2011 of small- and medium-sized enterprises (except for small- and medium-sized enterprises operating real estate business); enterprises producing, processing agricultural-forestry-fishery products, textile and garment, leather and footwear, electronic components, building socio-economic infrastructure that being labor-intensive shall be prolonged under the Prime Minister’s Decision No. 21/2011/QD-TTg Decision No. 54/2011/QD-TTg Decision No. 04/2012/QD-TTg.

4. If Enterprises being enjoyed enterprise income tax payment prolongation prescribed in Clause 1, Clause 2 above are being enforced to implement administrative decisions due to enterprise income tax debt, they are not subject to coercive tax payment within prolonged term of the enterprise income tax payment.

5. Small- and medium-sized enterprises operating the business of lottery, securities, finance, banking, insurance, or producing excise tax-liable goods, services (including other kinds of business); first-class, special-class enterprises belonging to Corporations or General companies, economic organizations being non-business units are not subjects of enterprise income tax payment prolongation.

Enterprises producing, processing agricultural-forestry-fishery products, textile and garment, leather and footwear, electronic components, building socio-economic infrastructure that demand labor-intensive ; enterprises producing mechanical products being means of production, means of waterway transportation, (including inland waterway and sea transportation), producing steel, cement that have other business activities (apart from business of lottery, securities, finance, banking, insurance, or producing excise tax-liable goods, services) are still entitled for enterprise income tax payment prolongation regarding the enterprise income tax amount not being remitted to the State budget as prescribed in this Article.

6. Enterprises are entitled for enterprise income tax payment prolongation prescribed in this Article are enterprises being established and operate under the Vietnam’s law, implementing the regime of accounting, invoices and documents under the law provisions, and paying tax under declarations.

7. Enterprises being subjects of prolongation prescribed in this Article must make Annex 2 (promulgated together with this Circular) and send to the direct management tax agencies specifying: the case which enterprise are subject of the enterprise income tax payment prolongation and the enterprise income tax amount being prolonged.

Article 4. Exempting license tax for fishing households and salt-producing households

Fishing households are exempted from the license tax in 2012. The tax payers eligible for tax exemption has paid license tax in 2012 shall be refunded the paid tax amount.

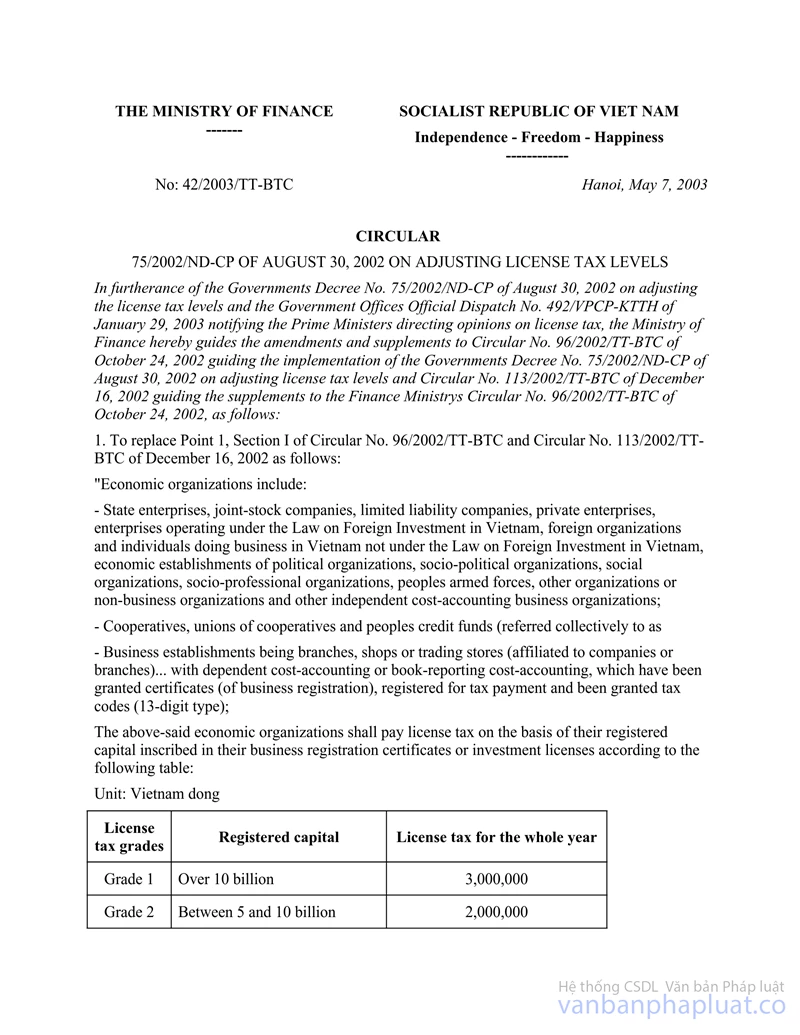

Salt-producing households are exempted from license tax as prescribed in point 3 of the Circular No. 42/2003/TT-BTC on guiding the amendment and supplement of the Circular No. 96/2002/TT-BTC of December 24, 2002 of the Ministry of Finance.

Pursuant to the approved register of license tax, before June 10, 2012, Sub-departments of tax shall make the list and determine the exempted tax amount of fishing households being subjects of license tax exemption in 2012 and being managed collection of tax by the tax Sub-departments, report to the district-level People’s Committee; the Director of the tax Sub-department shall issue decisions on license tax exemption in 2012 together with the list of households eligible for license tax exemption in 2012. The Sub-department of tax shall make the list of households eligible for tax refund in each district, issue Decisions on tax refund and cooperate with State Treasuries at the same level to implement the tax refund procedures regarding the tax amount being excessively paid through commune-level People’s Committees before June 15, 2012.

Basing on the list of license tax exemption and refund decided by tax agencies, commune-level People’s Committees shall notify the exempted tax amount to every tax payer and publicly post the list at convenient places. Commune-level People’s Committees are responsible to refund the paid license tax amount in 2012 to every household that pays tax before July 01, 2012.

Article 5. Prolongation of land levy payment

1. Subjects of application:

a) For economic organizations being investors of projects liable to pay land levies under the Notification of tax agencies or competent agencies but fail to pay or not fully pay until May 10, 2012, the longest land levy prolonged term is 12 months under the decisions of provincial-level People’s Committees and being started from May 10, 2012.

Economic organizations must continue paying land levies together with late payment fines after the land levy prolonged term is expired as prescribed in this point.

b) For economic organizations being investors of projects liable to pay land levies arising after May 10, 2012 until December 31, 2012 under the Notification of tax agencies or competent agencies, the longest land levy prolonged term is 12 months under the decisions of provincial-level People’s Committees.

The payment delaying is not fined within the land levy prolonged term prescribed in this Clause.

2. Basing on the actual difficulties of investors, the effect of the revenues from levy of the land of the infrastructural investment on local budgets, after obtaining opinions from the Standing People’s Councils at the same level, the provincial-level People’s Committees shall decide the land levy prolonged term particularly for each project or group of projects that the investors have not paid or fully paid. The prolonged term in maximum do not exceed 12 months.

3. Order, procedures and authority to prolong land levy payment:

a) Economic organizations being the subjects prescribed in Clause 5 of the Resolution No. 13/NQ-CP must send written requests specifying the financial difficulties to the Departments of Finance in central-affiliated cities and provinces attaching with the following relevant dossiers (verified photocopies):

- The Decision on land allocation to implement the project by competent State agencies.

- The Decision on approving the land price for land levy calculation, or the Decision on approving the land levy payable by competent agencies.

- The notification of land levy payment, fine for payment delaying (if any) by tax agencies or competent agencies.

- The documents (photocopies) and explanatory reports on the financial difficulties of the enterprise (if any).

b) The Departments of Finance in central-affiliated cities and provinces, within 10 days after receiving the application for land levy payment prolongation, shall cooperate with the Tax departments to review and make plans on proposal for particular prolonged term and submit to provincial-level People’s Committees.

c) Provincial-level People’s Committees shall base on the plans suggested by financial agencies and tax agencies to consider and report to the Standing People’s Council at the same level.

d) After obtaining opinions from the Standing People’s Council at the same level, provincial-level People’s Committees shall make decisions on the land levy prolongation.

dd) The Tax department shall implement in accordance with the decision on the land levy payment prolongation of the provincial-level People’s Committees.

Article 6. Effects

This Circular takes effect as from its signing.

If the contents in previous documents are contrary to the guidance in this Circular, the guidance in this Circular shall apply.

For VAT in the importation stage of machinery, equipment and specialized means of transport belonging to the technology lines and construction materials unable to be produced at home and needed to be imported to constitute fixed assets of the enterprises, the Circular No. 92/2010/TT-BTC of June 17, 2010 of the Ministry of Finance shall apply.

Article 7. Implementation responsibilities

People’s Committees of central-affiliated cities and provinces shall direct the functional agencies to implement in accordance with the Government’s provisions and the Ministry of Finance’s guidance.

2. Tax agencies at all levels are responsible to disseminate and guide organizations, individuals to implement in accordance with this Circular.

3. Organizations and individuals being subjects of regulation of this Circular shall implement in accordance with the guidance in this Circular.

Organizations and individuals are recommended to send feedbacks on the difficulties and obstructions arising during the course of implementation to the Ministry of Finance for study and settlement./.

|

|

FOR

THE MINISTER |

------------------------------------------------------------------------------------------------------

This translation is made by LawSoft,

for reference only. LawSoft

is protected by copyright under clause 2, article 14 of the Law on Intellectual Property. LawSoft

always welcome your comments